Money being counted at a bank's teller point. Photo/FREDRICK ONYANGO

Tech-savvy bank employees who turn work stations into stealing grounds now pose the greatest risk to the industry, a new survey shows.

The thefts have been made easy by Internet banking, which allows fraud at the click of a mouse.

Consultancy firm PricewaterhouseCoopers (PwC) said that bank employees—who stole more than Sh2 billion from banks last year—pose the largest threat to banking profitability ahead of competition from rivals and risk of default by borrowers.

These employees have been supported by heavy automation of the banking industry over the past two years as local players move to embrace Internet and mobile banking services.

This in turn has enabled workers to siphon billions through electronic funds transfer, fraudulent loan applications and cheque fraud.

While banks thought the enhanced IT platforms would help them cut costs and enable customers’ access services from the comfort of their homes, PwC says the benefits of these intentions have been wiped out by the fraudsters.

“Technological advances, while necessary, have made banks’ businesses more vulnerable. As systems become more complex, the opportunities for fraud increase,” says the consultancy firm on Wednesday in report accessing the risks facing regional banks.

“We’re seeing more and more cases of fraud perpetrated by insiders—disgruntled or disillusioned employees who are usually young and more tech-savvy than their superiors,” added PwC.

This is the first report to link banking employees to the soaring cases of fraud as executives in the industry has preferred to remain silent on the issue to protect their reputation and avoid bad publicity from the courts.

Cheque fraud, electronic fraud, cash fraud, impersonation fraud such as with credit card theft, fraudulent loan applications and personal information theft are some of the current trends in fraud and are exacerbated by technology advances, competition and a rapidly evolving marketplace.

Colluding

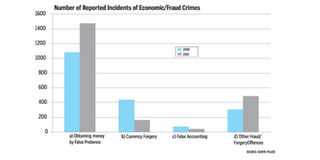

Banking Fraud Investigations Department (BFID) says cheque fraud tops the list of commercial crimes tabulated by the banking sector followed closely by the Real Time Gross Settlement (RTGS) - transfer of funds from one bank to another in real time.

It says bank employees are fast joining an international syndicate of fraudsters by either providing insider information or colluding with clients to siphon money.

The BFID says that banking fraud more than tripled in the third quarter of 2010, to Sh1.7 billion, with the staff involved in the bulk of the fraudulently dealings.

With bank staff able to access account details and see the number of the last cheque cleared, many are now having forged cheques drawn up, which they are then presenting for encashment, often on dormant accounts.

Industry insiders say the reported cases also represent only a fraction of the actual fraud.

“Many banks do not make full disclosures of what has been stolen because they think it is bad publicity,” said the head of security of one of the banks.

Most Kenyan banks have in the past two years introduced electronic banking products that have not only increased the efficiency of transactions but also significantly reduced the number of people going to the banking halls for services.

They have also revamped the core banking systems—spending between Sh600 million and Sh750 million—in what has reduced the need for paper work and backroom offices due the automation of branches, which has rendered a number of workers redundant.

Central Bank of Kenya (CBK) says the number of commercial banks offering electronic banking services stood at 33 out of the 44 as at December 31, 2009.

The heavy investments in IT have been driven by the need to keep a lid on costs without compromising the need for the banks to boost their reach in a competitive banking market.

Enhanced ICT platforms are also helping banks to introduce internet and mobile banking services that enable customers to check their statements of accounts, make inquiries on status of cheques, cheque book requests, transfer of funds between designated accounts and make utility payments.

This has reduced the need for more staff and branches to reach customers.

But PwC reckon that bankers are dropping their guards when it comes to matters security.

“Fears about inadequate resources and commitments to safeguarding information and processes may inflate the feeling of risk associated with a high dependence on technology,” says the consultancy firm.

The chief executive of the Kenya Bankers Association (KBA), Habil Olaka, said the industry is feeling the heat on the rising fraud cases.

KBA is calling for thorough vetting of staff and tightening of bankers’ internal securities.

Mr Olaka says that the industry is counting heavily on the new cheque truncation process, which is an electronic and automated system of handling cheques, to eliminated fraud.

“Cheque truncation will reduce the clearing cycle and eliminate fraud brought by cheque substitution,” said Mr Olaka.

But banks have also moved to beef their security desks hiring former detectives to tame the vice that is threatening earnings.

Kenya Commercial Bank, Consolidated Bank, NIC Bank and National Bank of Kenya are some of the institutions that have hired security and fraud experts.

“We have also invested heavily in other preventive measures, alongside thorough vetting of our employees,” said NIC Bank managing director, James Macharia in an earlier interview.

“We have been increasing our training budget by about 20 per cent ever year to ensure that our staff is up to date with the latest threats and technology advances.”

Forensic

But BFID further says that forensic auditing sections often fall under either internal audit or security department in some banks, which compromises their independence and integrity.

It recommends setting up of independent forensic units within the banks.

The implementation of the Credit Reference Bureau system has also been hailed as a stepping stone to curbing the deluge of fraud, by helping address fraud by customers as banks share information on previous banking records.

The banks have yet to move to any formal sharing of information on banking staff.

However, the provisions of the Anti money Laundering Act, which came to effect on 28th June last year, should also now help in tracking down fraudsters.

The Act requires financial institutions to submit suspicious transactions and Cash Threshold Reports to the Financial Reporting Centre, which will then be used to facilitate the gathering of financial intelligence for analysis.