Low capital slows down Islamic banks’ earnings growth

Gulf African Bank reported its slowest growth in profit for 2013. Photo/FILE

What you need to know:

Analysts in part attribute the performance of the Shariah-compliant lenders to their weak capital base that hampers their ability to grow their loan books and lend to corporates.

Islamic banking is based on Islamic law (Shariah) where interest is forbidden and deposits are only invested in Sharia-acceptable deals which exclude those involving alcohol, pork and gambling.

Shariah-complaint banks lend to both Muslims and non-Muslims and make money from fees and commissions on lending and other products such as asset financing, mortgages, takaful (Islamic insurance) and local purchase orders financing.

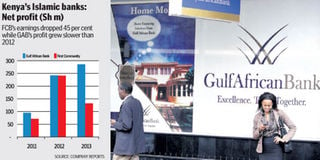

Islamic banks reported declining fortunes last year with First Community Bank’s (FCB) net profit plunging by nearly half and Gulf African Bank (GAB) reporting slower growth in earnings, reversing a trend where they recorded triple digit growth in 2012.

FCB saw its full-year after-tax profit dip 45.2 per cent to Sh132.2 million from Sh241.3 million in 2012, impacted by flat operating income from fees and commissions on lending and higher expenses on deposits.

The lender earnings grew more than threefold in 2012 when its profit jumped to Sh241.3 million from Sh71.3 million in 2011 on the back of aggressive lending to households.

GAB posted a 17.9 per cent growth in net profit to Sh285.5 million in the year to December 2013 compared to Sh242.2 million a year earlier despite a drop in income from loans.

It saw net profit more than double in 2012 to Sh242.2 million from Sh95.3 million of previous year.

Analysts in part attribute the performance of the Shariah-compliant lenders to their weak capital base that hampers their ability to grow their loan books and lend to corporates.

“FCB has a small balance sheet which has made it focus on the mass market. It should engage institutional investors to raise capital and lend to corporates,” said Raymond Nyamweya, a financial consultant at Rose Avenue Consulting Group.

“GAB needs to enhance its capital to lend more as income comes from financing activities.”

Kenya’s banking laws cap lending to a single borrower at 25 per cent of a bank’s core capital.

This means that FCB can loan up to Sh285 million and GAB can lend up to Sh667 million based on their core capitals of Sh1.1 billion and Sh2.6 billion respectively.

FCB’s loan book expanded by Sh1.7 billion to hit Sh7.2 billion while GAB’s grew by Sh1.2 billion to Sh10.6 billion.

“In 2012, we disposed a property for Sh134 million and this was a one-off income that increased earnings. There are plans to increase core capital to fund growth,” said Omar Sheikh, general manager at FCB Group.

Islamic banking is based on Islamic law (Shariah) where interest is forbidden and deposits are only invested in Sharia-acceptable deals which exclude those involving alcohol, pork and gambling.

Shariah-complaint banks lend to both Muslims and non-Muslims and make money from fees and commissions on lending and other products such as asset financing, mortgages, takaful (Islamic insurance) and local purchase orders financing.

The slowdown by the two lenders comes at a time when conventional lenders such as Barclays, Standard Chartered, KCB, National Bank, Chase are revamping their Islamic banking products to capture Kenya’s sizeable Muslim population.

GAB began operations as a commercial bank in 2007 to be Kenya’s first fully-fledged Islamic bank and currently has 14 branches.

It is 90 per cent owned by group of institutional investors including the International Finance Corporation (IFC), Dubai-based private equity firm Istithmar World, Bahraini lender BMI Bank, Saudi billionaire Sheikh Abdallah Mohammed Al Romaizan and Dubai investment firm GulfCap.