Entrance to the East Africa Portland Cement factory in Athi River. Inset, Mr Simon Peter ole Nkeri, MD of EAPCC and Mr Kephar Tande, the former MD. PHOTO | FILE

What you need to know:

Audit says Portland’s current liabilities of Sh4.96 billion have grossly exceeded its current assets of Sh2.11 billion, leaving it technically insolvent.

It also found operational gaps that may have been exploited by unscrupulous employees to enrich themselves, raising the possibility that its stocks have been overstated by Sh791 million.

Auditor-General Edward Ouko has offered a gloomy assessment of East African Portland Cement Company (EAPCC), casting doubts on the firm’s ability to stay afloat with a Sh2.8 billion hole in its balance sheet.

Mr Ouko, in an audit report prepared on his behalf by consultancy firm Deloitte, says that Portland’s current liabilities of Sh4.96 billion have grossly exceeded its current assets of Sh2.11 billion, leaving it technically insolvent.

This means that if EAPCC creditors recalled their liabilities today, the State-owned cement firm would not be in a position to settle them within one year.

Deloitte’s report, which covers the year to June 2016, is the reason Portland did not release its financial results on time, indicating that its net profit nearly halved to Sh4.2 billion due to a Sh1 billion dip in the value of its property after revaluation.

The audit also found operational gaps that may have been exploited by unscrupulous employees to enrich themselves, raising the possibility that its stocks have been overstated by Sh791 million.

The list of questionable deals at EAPCC includes unexplained expenses on stock purchases, the chaotic exit of employees who were paid millions of shillings in salary advances as well as money that was received but not allocated to specific transactions.

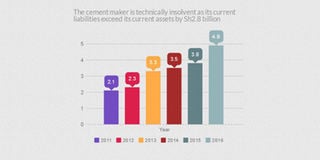

“The group incurred a loss from operations of Sh1.68 billion during the year ended June 30, 2016. As of that date, current liabilities exceeded current assets by Sh2.84 billion,” Mr Ouko says in a letter acknowledging receipt of the audit.

“These conditions along with other matters indicate the existence of a material company uncertainty which may cast significant doubt on the group’s ability to continue as a going concern.”

Mr Ouko, who received the report on November 8, did not immediately respond to questions on his opinion.

Portland is a public company in which the Treasury has a 25 per cent stake and the National Social Security Fund 27 per cent. LafargeHolcim has a 41.7 per cent stake.

Fixing loopholes

When contacted for comment, the Portland management confirmed having received the audit report.

“Management is aware of the potential technical insolvency where the current liabilities exceed current assets by Sh2.8 billion,” the firm said in an email response to the Business Daily queries.

The cement maker said efforts were ongoing to fix loopholes in its operating system.

“A reconciliation of the general ledger to the sub ledger (is ongoing)… this is expected to be completed by June 2017,” said the company.

The larger portion of Portland’s current liabilities is in trade and payables -- money it owes suppliers – totalling Sh2.5 billion while the rest is made of unpaid dividends, bank overdraft and part of a long-term debt.

Its current assets are made up of bank balances and cash, inventories, trade receivables, short-term deposits, amounts due from a Ugandan subsidiary and recoverable taxation.

While flagging the cement maker’s precarious financial position, Deloitte encountered glaring system cracks it says may have been used to fleece the company.

Top on the list of worrying revelations is a stock count which “yielded differences between the inventory physically counted and the amounts recorded in the general ledger.”

The discrepancy was so significant that Portland has now made a Sh791 million provision in its financial statement, an indicator that the stocks may not be recoverable.

“A comprehensive analysis of the source of the variance would allow management to identify how they arose – whether due to fraud or error,” Deloitte noted in its report.

The auditors also noted that the cost of some spare parts had been inflated.

In one case, an item whose actual cost was Sh1.93 million had been recorded as Sh19.2 million, indicative of possible fraudulent dealings. Yet another worrisome finding was unapplied receipts totalling Sh1.7 billion.

An unapplied receipt is one where the customer who submitted a specific payment has been identified but the receipt has not been linked to a specific transaction.

This leaves an open door for corrupt individuals to cart away stock from Portland’s warehouses and irregularly allocate these “sales” to the invoices already honoured.

“The existence of the unapplied receipts makes the company susceptible to fraud. In not matching receipts to invoices in a timely manner, the credit control function is ineffective,” Deloitte said.

Portland could also not account for Sh145 million in stocks for which it made a prepayment more than one year ago.

These raw materials were adjusted for during the audit, a move which illuminates loose stock-taking and accounting practices at the firm.

EAPCC is not new to reporting and accounting problems, with the more notable case happening at the December 2013 annual general meeting when majority shareholders Treasury and the NSSF raised audit queries.

The stormy shareholders meeting saw the two top shareholders claim the company’s management had cooked its statement of accounts and that the firm was “in the red”.

The boardroom wrangles culminated in the exit of the company’s chief executive, Kephar Tande, in June and his replacement, Simon Peter Ole Nkeri, was appointed a month later.

PAYE Tax Calculator

Note: The results are not exact but very close to the actual.