The entry of new cement makers has seen the bigger players cede significant market share as their cement is cheaper. Photo/FREDRICK ONYANGO

Cheaper pricing has won newly set up cement manufacturers about 14 per cent market share from their rivals, signalling a deepening shift in the industry that has for years been dominated by three producers.

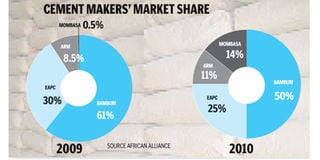

Industry statistics by African Alliance Investment Bank show that Mombasa Cement and National Cement—both established in the past two years—now control a combined market share of more than a 10th of the local cement market.

Bamburi Cement, which accounted for 61 per cent of cement sold in the market in 2009, has seen its market share drop to 50 per cent, while East African Portland Cement Company (EAPCC’s) market share has fallen by five per cent to 25 per cent.

Athi River Mining (ARM) has, however, recorded a marginal gain according to the African Alliance data, edging up by 2.5 percentage points to 11 per cent.

The three manufacturers are listed at the Nairobi Stock Exchange.

“The entry of these new cement makers has seen the bigger players cede significant market shares as their cement is cheaper,” said Francis Mwangi, a research analyst at African Alliance.

National Cement is currently selling a 50 kilogramme bag at Sh660, EAPC Sh650 and Bamburi Sh700 on its regular brand—Nguvu.

Mombasa Cement’s retail price is Sh600, while the lowest brand is ARM’s rhino cement retailing at Sh670 per bag.

Mr Mwangi said the new players have stolen significant market share of the bigger players including Bamburi and East African Portland Cement Company, riding on a pricing strategy.

Mark ole Karbolo, the chairman of EAPCC, termed the new cement manufacturers’ pricing strategy as “unsustainable,” adding that the new players are not likely to uphold their price undercutting for long.

Established network

“You cannot offer a superior product at the price of a regular product and expect it to survive for long,” said Mr Karbolo, whose firm is estimated to have lost about a sixth of its market share as per the African Alliance data.

Fortunes of the two new entrants have been buoyed by their established distribution networks, having already been players in the manufacture of other building materials including steel, nails and roofing sheets.

Mombasa Cement is owned by Uganda-based Tororo Cement, while National Cement is owned by Devki Group.

The holding company for Mombasa Cement, Corrugated Sheet, has been in the market for over a decade manufacturing a wide range of products under the nyumba brand, and has an established a distribution network across the country.

Devki on the other hand is a household name in the local construction industry after dealing in the manufacture and supply of steel bars and pipes.

Raval Narendra, the group managing director of the Devki Group, said his firm was keen on growing its market share to double digits this year.

“Our cement is superior because it dries fast and we are able to sell it at the same price, we are targeting a double digit market share this year,” said Mr Narendra.

A boom in the construction industry has seen a sharp increase in the demand for cement, an opportunity that the new players rushed in to gain from by diversifying their product offering.

Data from the Kenya National Bureau of Statistics indicates that cement consumption for the first nine months of last year was higher by about 245,000 metric tonnes.

Mr Mwangi said the increased consumption meant a bigger pie for all the players, but how the market share would turn out is still likely to change this year since the players are still very new.

“We can expect some market shifts this year before the market finally settles,” he said adding that the demand for cement is likely to increase even further.

Increased competition has seen older players diversify as they seek to cushion their earnings.

EAPCC announced plans to start making paving blocks and kerbs, following in the steps of the Bamburi which makes five variants of cement, paving blocks and plastering dust.

Surendra Bhatia, deputy managing director of ARM, said that new entrants are making big leaps due to use of new technologies.

He said newer mills have lower maintenance costs while they enjoy higher energy efficiency which helps them cut on their production costs and compete favourably.

“New technology can save as much as a quarter on energy costs which is very significant in cement production,” said Mr Bhatia. Energy costs account for about a fifth the production costs of cement while clinker- a mineral input in cement manufacture account fro up to half of the costs.

Kaushit Pandit, the director of sales at Mombasa Cement, said his firm has been able to pass on savings on energy, clinker and distribution to the end consumer in the form of cheaper products.

“Competitive price to our customers is the only reason we have been able to grow that fast,” said Mr Pandit, who said his company has more than 15 per cent of the market share.