Resumed oil exports by S. Sudan present opportunities and challenges

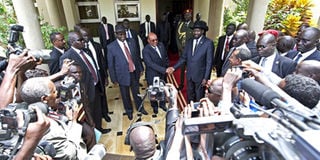

South Sudan’s President Salva Kiir and Sudan’s President Omar al-Bashir (left) shake hands at the State House in Juba last Friday. Mr Bashir visited South Sudan for the first time since 2011 , a sign of easing tension after bloody border battles last year. FILE

What you need to know:

New deal promises regional security but may require rethink of key LAPSSET component.

The recent diplomatic overtures between Juba and Khartoum are an indication that the two counties are now ready to co-operate economically to implement the agreement signed in September 2012.

Juba will resume production and exports of oil through Sudan, while Khartoum will earn revenues from use of its existing oil export infrastructure. A visit by President Omar al-Bashir to Juba last week makes us believe that this time around there is seriousness and commitment to work together for mutual benefits irrespective of outstanding political differences.

Prior to oil production shutdown in January 2012, the Khartoum government had decreed an oil export transit fee of about $32 per barrel to be paid by South Sudan for using its export logistics facilities.

The figure finally negotiated is between $9 and $11 per barrel depending on crude oil grade and source. Juba will additionally pay lump sum compensation to Khartoum for lost revenues.

What was interesting to note was that the absence of 350,000 barrels per day (bpd) of South Sudanese oil from global markets had very little if any noticeable impacts on global oil supply/demand balance and prices.

Oversupply of oil by other countries, and reduced demands in others were able to smoothly accommodate production shortfalls from South Sudan.

At the diplomatic level, we have seen that the African Union has come of age as they patiently and effectively negotiated the September 2012 peace and economic co-operation deal between the two countries.

The oil exports closure for over one year has given the two countries time to re-evaluate their economies in the absence of oil revenues. The North was able to look at other sources of revenue by developing other resources, including gold.

The South, faced by a serious budget deficit, re-examined how efficiently they spend money and I am sure they plugged a number of cashflow leakages. The South may also have paid serious attention to developing the non-oil economic sectors.

The resumption of oil exports by South Sudan will have implications on the region and on Kenya in particular. First and foremost the struggling Kenyan businesses already in South Sudan expect a revival with increased foreign exchange inflows into the economy.

The Khartoum/Juba agreement, if it proves sustainable, will attract even more regional and international investments. There is the pending membership of EAC which will formally open up South Sudan to more regional trade and protocol.

On its part the Juba leadership will need to conclusively establish sustainable security within its borders to attract and maintain investments and donor development funds.

During the period the Sudanese oil supply systems have been closed down, oil products ceased to flow from the Khartoum refinery to the South.

Kenya stepped in with supplies of products from Eldoret, at a time when Kenya Pipeline Company had just increased its capacity by commissioning a new larger pipeline from Nairobi to Eldoret.

It can be expected that products loadings from Kenya will gradually reduce as supplies from Khartoum via the River Nile barges resume. It is understood that in the medium term, South Sudan plans to put up a refinery north of Juba to meet local demand for oil products and reduce reliance on imports.

Alternative routes

Consideration for alternative routes for oil export by the South can now be undertaken in a less subdued atmosphere. It should be an alternative pipeline justified more by logistics needs and good economics than merely on political fears of insecurity. Juba has been exploring alternative oil export routes through the LAPSSET project in Kenya and also through Ethiopia.

The acronym LAPSSET has “SS” in it because of South Sudan. The LAPSSET project petroleum infrastructure components (pipelines and refinery) were essentially justified on the basis of availability of crude oil from South Sudan.

This was at a time when pessimism existed (prior to the separation of the two countries in 2011) that Khartoum and Juba were highly unlikely to co-operate politically leaving alone economically. This pessimism is still under test.

As of now, the LAPSSET petroleum infrastructure model can be maintained only if Kenya confirms commercial volumes of oil discoveries in the north west of Kenya, and/or the Ugandans opt to link up and jointly export their crude oil production through Lamu.

The Ugandan upstream oil investors still have to evaluate the economics of other alternative routes through southern Kenya, and northern Tanzania.

In addition to reviving the existing oil production facilities, South Sudan will as early as possible need to step up exploration of new acreage for more oil as current wells are understood to be experiencing production declines. Establishing sustainable security will be paramount in determining the pace of new capital inflows in the upstream oil and gas sector.

New oil will ensure that the country does not lag far behind in light of the major efforts that are already transforming the eastern parts of Africa into a significant global oil and gas exploration and production arena, which includes Mozambique, Tanzania, Uganda, Kenya, Somalia and Ethiopia.

For the EAC countries we can only hope that Khartoum and Juba will in future embrace permanent peaceful political co-existence and economic co-operation by diplomatically and responsibly resolving outstanding issues. This should go a long way in establishing sustainable security within South Sudan.

Wachira is the director, Petroleum Focus Consultants. [email protected]

PAYE Tax Calculator

Note: The results are not exact but very close to the actual.