Rapid growth of banks puts to test industry stability

Central Bank of Kenya in Nairobi. CBK governor Prof Njuguna Ndung’u said it was normal for the banking industry to pull ahead of the rest of the economy. Photo/File

What you need to know:

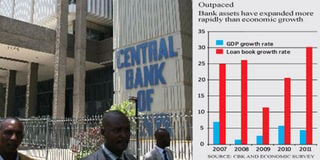

As at September 2012, the banking sector had grown its asset base by 13.8 per cent, while the economy expanded by 4.5 per cent in the same period.

The sector has recorded double-digit growth in profits for most of the past decade, when the economic growth has averaged at about five per cent.

A banking sector growing faster than the rest of the economy could result in institutions and households that are not able to repay their debts leading to growth of non-performing loans.

Rapid growth of the Kenyan banking sector, which has outpaced overall economic growth in the past decade, is likely to test the industry’s stability as borrowers find it hard to keep up re-payments of their loans.

South African based research and stockbrokerage firm, Legae Securities, has pointed out that the difference between the growth of Kenya’s banking industry and the national economic expansion (GDP) is not well balanced and could require banks to hold higher capital buffers to absorb possible shocks.

A banking sector growing faster than the rest of the economy could result in institutions and households that are not able to repay their debts leading to growth of non-performing loans, analysts at Legae have warned.

“The natural long-term growth rate of assets in a system is (at the same rate as) the nominal GDP growth rate or somewhere around there. However, in Kenya, bank asset growth has significantly outpaced nominal GDP. We are concerned that the divergence is excessive,” reads part of the report which compares Kenya’s and Nigeria’s banking sector.

As at September last year, the banking sector had grown its asset base by 13.8 per cent, while the economy is estimated to have expanded by 4.5 per cent in the same period.

The banking sector has recorded double-digit growth in profits for most of the past decade, when the economic growth has averaged at about five per cent.

The South African analysts said that Kenyan banks could be managing their loan portfolios by either writing off the bad loans and absorbing the losses, restructuring the loans so as not to capture them as bad loans, or slowly disposing securities so as to cover for defaulted instalments ensuring a loan does not slip to bad books.

Provisioning of bad loans has been an issue in the Kenyan banking sector after Citi Investment Research accused the sector last year of under-providing for bad debts to inflate their profit levels.

A loan that goes for three months without being serviced should be classified as non-performing and 20 per cent of it or more should be set aside by the bank as cushion in case the full amount is unpaid. The amount set aside impacts on a bank’s profits as it is a deductable expense.

In a presentation to members of accounting body, ICPAK, Central Bank governor Prof Njuguna Ndung’u had in July last year sought to justify the sector’s growth stating that it was normal for the industry to pull ahead of the rest of the economy.

“As the economy continues to recover and the government is rolling out infrastructure projects to increase the capacity for future economic growth, the financial sector will thrive,” said Prof Ndung’u.

Vimal Parmar, the head of research at Burbidge Capital said the rapid growth should not be a concern as it was as a dividend of financial inclusion.

“From where we were coming the market was quite unbanked so penetration leads to growth and in this case most of the banks have taken in high quality assets,” said Mr Parmar.

Legae Securities, however, hold that the very increase in penetration of banking services could lead to a drop in the credit multiplier, a measure of the relationship between asset growth and nominal GDP growth in a system.

“As penetration increases, the multiplier should naturally decline, otherwise a continued discrepancy between nominal GDP growth and system asset growth will eventually have one chief effect —pressure on asset quality,” said Legae Securities.

The quality of the bank loans has been improving with 4.6 per cent of the loan book classified as non-performing equivalent to Sh57.7 billion as at September last year compared to a ratio of nine per cent in September 2007 at Sh59.1 billion.

The drop in total non-performing loans has been a source of concern as market observers question how the banks have grown their loan books without recording increase in bad loans.

“The growth of non-performing loans should match the gross loans which has not been happening so going forward this will be a concern,” said Mr Parmar, echoing Legae Securities’ observation.

James Mwangi, the chief executive of Equity Bank has in the past dismissed the reports by international research firms saying they had an underlying intention.

The international analysts have been recommending Nigeria banking segment, which is rising from the throes of collapse, as a better investment option.