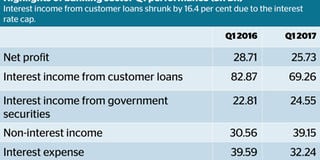

The reports show that the banks earned Sh69.26 billion in interest from customer loans in the first three months of the year, down 16.4 per cent from Sh82.87 billion in the first quarter of 2016.

The lower earnings have led to massive job losses in the sector as banks try to control costs.

Loanbook growth in the first quarter trailed that in customer deposits, which went up by 7.9 per cent to Sh2.94 trillion, equivalent to a rise of Sh214.5 billion.

The law capping interest rates slashed Sh13 billion of commercial banks’ interest income from customer loans between January and March, fresh data released by the lenders shows.

The first quarter performance reports, which all banks were required by law to have released by May 31, signal a year of leaner earnings for the lenders this year.

The reports show that the banks earned Sh69.26 billion in interest from customer loans in the first three months of the year, down 16.4 per cent from Sh82.87 billion in the first quarter of 2016.

The fall in interest earnings, which constituted 62 per cent of operating income for banks during the quarter, led to a Sh3 billion fall in the banks’ net profit to Sh25.7 billion.

Banks were expected to take a hit in income following the capping of interest rates on customer loans at four percentage points above the prevailing Central Bank Rate, which currently stands at 10 per cent.

The lower earnings have led to massive job losses in the sector as banks try to control costs.

It has also led to a slowdown in the physical expansion that banks had announced recently, with the lenders instead turning to cheaper alternative banking channels.

Experts are warning that there is unlikely to be respite for the lenders in the short term, with the interest rate cap, which is popular with members of the public, unlikely to be revised in an election year.

This is in spite of indications from the Treasury and the Central Bank of Kenya (CBK) that they would favour a review, and calls from the International Monetary Fund (IMF) to scrap the rate cap.

Those in favour of the caps, however, argue that the banks’ profitability will stabilise after adjustment of their cost structures and ultimately benefit the overall economy through lower cost of loans.

“In terms of timing, we do not think there is sufficient time for the reversal to be passed by Parliament as it will be dissolved in June ahead of the elections in August.

We think the most appropriate time to introduce a reversal will be in the 2018/19 Fiscal budget implemented between July 2018 and June 2019,” said Exotix Partners analysts Ronak Gadhia and Muamar Ismaily in a banking sector update.

“Given the regulatory hurdles the banks are facing over the next two years, we estimate that the deceleration in earnings growth and decline in return on equity could continue for a further two years.”

Proponents of the rate cap review would, however, face an uphill task of convincing Parliament to effect the change of law, which came about from a private member’s Bill.

The decline in interest earnings is also a factor of a flat loan book, which grew by only 0.7 per cent or Sh15.2 billion year-on-year to stand at Sh2.356 trillion at the end of March.

Banking sector Q1 performance.

Deposits growth

Loanbook growth in the first quarter trailed that in customer deposits, which went up by 7.9 per cent to Sh2.94 trillion, equivalent to a rise of Sh214.5 billion.

Banks have significantly cut back lending to customers since the rate cap law came into force, and have instead been competing to lend to government.

They reported net investments in government securities of Sh846.5 billion by the end of March, which was a Sh109 billion increase over one year.

Interest earnings from government securities in the period rose from Sh22.8 billion to Sh24.6 billion.

The lenders have also turned to transactional income to fill the gap in interest income.

The industry’s non-interest income rose by 28 per cent to Sh39 billion in the first quarter of the year, led by tier one lenders Standard Chartered #ticker:SCBK, Equity Bank #ticker:EQTY, KCB #tickerKCB and Commercial Bank of Africa.

Technology investment These banks have recently invested heavily in technology, opening new lines of revenue from transaction fees.

KCB and CBA have partnerships with telecoms operator Safaricom #ticker:SCOM to offer mobile-based loan products, while Equity runs its own Equitel platform for the same.

Bank owners are also feeling the heat of lower profits, with the industry’s return on equity (RoE) shrinking by five percentage points since June last year.

Kenyan banks have for long been some of the most profitable in the world, with returns per shilling invested for large lenders averaging 25 per cent to 30 per cent between 2010 and 2015.

CBK Governor Patrick Njoroge said last week that the industry RoE fell to 13.6 per cent in March from 18.2 per cent in June.

Tier one RoE shrank from 34.7 per cent to 23.1 per cent.

“These numbers falling reflects the lower levels of profits in some of these institutions,” said Dr Njoroge.

PAYE Tax Calculator

Note: The results are not exact but very close to the actual.