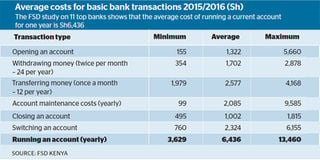

Standard Chartered’s ordinary current account was found to be the most expensive among the 11 sampled – coming with a yearly running cost of Sh13,460 or an average of Sh1,120 per month.

Co-operative Bank #ticker:COOP levies customers Sh3,629 a year, or Sh302 per month, making it the cheapest on account charges.

There's added emphasis on fees and commissions as an alternative source of income to cover for the drop in interest income after the rate capping law.

Standard Chartered Bank’s #ticker:SCBK current account customers pay the highest maintenance and transaction costs among Kenya’s big banks, a newly released report shows.

The report, which is the product of a two-year survey of the banking market by Financial Sector Deepening (FSD) Kenya, indicates that some bank customers are forced to pay up to Sh14,000 a year in account maintenance fees alone, adding to the cost of accessing financial services.

Standard Chartered’s ordinary current account was found to be the most expensive among the 11 sampled – coming with a yearly running cost of Sh13,460 or an average of Sh1,120 per month.

Co-operative Bank #ticker:COOP levies customers Sh3,629 a year, or Sh302 per month, making it the cheapest on account charges.

“A customer who withdraws twice per month, transfers money once a month and pays for basic account maintenance (ledger fees, mini-statements, card replacements) can pay between Sh3,629 to Sh13,460,” said FSD in its annual report for 2016.

“The major difference between accounts depends on the fixed “account maintenance” costs. While many banks offer a pay-as-you-go option for their key retail accounts, some offer only premium solutions with relatively higher monthly ledger fees.”

Other banks whose charges were sampled for the study are KCB #ticker:KCB, Equity Bank #ticker:EQTY, Barclays #ticker:BBK, DTB #ticker:DTK, Family Bank, Commercial Bank of Africa, NIC Bank #ticker:NIC, National Bank #ticker:NBK, and Stanbic Bank #ticker:CFC.

These banks together accounted for 96.5 per cent of the industry’s 34.6 million deposit accounts at the beginning of 2016, and collectively held a 73.4 per cent share of the banking sector market, according the latest available CBK statistics.

The FSD survey sampled the charges levied on a total of 22 different current and salary accounts in each bank.

Barclays’ Ultimate account and Stanbic’s Smart Banking account charge about Sh12,000 and Sh10,000 per year respectively, placing them among the most expensive when it comes to account charges.

Co-operative Bank’s salary account and KCB’s Jiinue and Bankika accounts were, however, found to attract the lowest annual charges of below Sh4,000.

FSD said information on the various charges was hard to come by, and that some bank staff advised customers on the type of account to open based on their (customer’s) source and level of income rather than need.

Most bank customers were found to be largely unaware of the charges for some less common transactions such as bank-to-mobile transfers, salary processing fees and inward transfers from other banks. PHOTO | BD GRAPHIC

In some banks, staff would make an effort to sell to customers a charged account even when they specifically asked for a tariff-free option.

Customers unaware of levies

Most bank customers were found to be largely unaware of the charges for some less common transactions such as bank-to-mobile transfers, salary processing fees and inward transfers from other banks.

“Our mystery shoppers had to make up to six visits per bank as well as consult tariffs posted at branches and on websites, to understand the cost of a transaction,” said FSD.

In addition to the high tariffs on customer accounts, banks also make a tidy sum from processing fees on customer loans.

Banks have since September last year been boxed into a rate cap of 14 per cent, a move that has directly affected their interest income, which has been their largest source of revenue.

This has led to added emphasis on fees and commissions as an alternative to cover for the drop in interest income, combined with aggressive cost cutting.

The large banks are charging higher fees on customer loans compared to their smaller rivals, with some taking their Annual Percentage Rate (APR) or total cost of credit to over 20 per cent.

The recently launched Kenya Bankers Association (KBA) cost of credit website shows that a one-year Sh1 million unsecured loan from Barclays would cost a borrower Sh135,245, which includes a Sh57,800 fee that is equivalent to 42.7 per cent of the total cost of credit.

At Equity, the charges would amount to Sh55,000, accounting for 41.5 per cent of the total cost of credit of Sh132,445.

The KBA data shows that the higher cost of credit arises from the numerous and larger non-interest charges, including appraisal and processing fees, on the loans.

Banking sector data compiled by the Business Daily shows that in the one year to March 2017, banks were able to grow their non-interest income by 28.1 per cent to Sh39.14 billion, compensating for a 12.1 per cent fall in interest income to Sh95.7 billion in the period.