Individuals found in breach of the rules will pay a higher fine of Sh1 million up from Sh200,000.

The proposed measures are contained in a letter that the CBK has written to chief executives of banks asking for their input by the end of this month.

Dr Njoroge insisted banks need to review and scrap all “nuisance fees”, saying such moves have had a significant negative effect on customers.

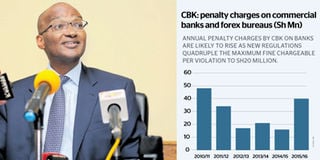

The Central Bank of Kenya (CBK) has published new regulations quadrupling the penalties that commercial banks will pay for failing to disclose the true cost of credit to customers, sustaining the pressure on the lenders already feeling the heat from the law capping interest rates.

The draft regulations on penalties for banks, mortgage companies and credit reference bureaus indicate that the CBK will impose the maximum penalty of Sh20 million for every violation arising out of customer complaints on charges and other cases of non-compliance with the Banking Act and Prudential Guidelines.

“Specific violations, which may be subject to assessment of monetary penalty under these regulations, include paying interest or return on deposits below the prescribed statutory minimum; failure to disclose total cost of credit or charges to a customer; imposition/increase of any charge on any product or service without prior written approval,” the CBK regulations say.

The new rules are meant to bring into force the Finance Act of 2016 that increased the fines for violation of the laws from the previous Sh5 million.

Individuals found in breach of the rules will pay a higher fine of Sh1 million up from Sh200,000.

Non-compliant banks will also pay aggravated daily penalty of Sh100,000 from Sh20,000 till the day of full compliance.

The new rules promise greater protection to bank customers, who have been suffering from arbitrary increases in charges and interest on loans as well numerous fees hidden in fine print.

The CBK says the penalties prescribed under the regulations will apply “to each and every violation and assessment of the penalty may be carried out for each and every single violation.”

The previous law was silent on whether a fine imposed on a bank with multiple violations would be assessed individually or collectively.

Penalising violations individually could leave banks with huge bills in the event of complaints by a large number of customers.

The CBK, however, says any fine imposed will take into account the financial condition of the institution being fined so as not to paralyse it as a result.

The lenders will also face fines for charging interest on loans or other credit in excess of the prescribed statutory maximum and for recovering interest or other charges on non-performing loans in excess of the prescribed limit.

A number of banks have recently been reported to have sent notices to loan defaulters warning them that they would be hit with levies above the legal cap of 14 per cent, causing fear across the entire industry.

The rate cap law that came into force last September is silent on levies to be charged on defaulters, a position the banks saw as a loophole to charge additional interest on credit.

The proposed measures are contained in a letter that the CBK has written to chief executives of banks asking for their input by the end of this month.

They came to light on the same day CBK governor Patrick Njoroge disclosed yesterday that the regulator had rejected 13 out of 16 commercial bank request for permission to increase charges.

“Since September 2016 we have had something like 16 requests for fees, imposition of a fee or adjustment in fees or request for approval for fees. We have only approved three,” said Dr Njoroge at a press briefing in Nairobi.

“Those three (requests) have been new services, new products. We are holding the other 13 (requests) in abeyance.”

The banks’ quest to impose higher levies is typical of their reaction to the rate cap law, which has cut interest earnings, leaving higher fees and commissions as the only means of growing income from lending operations.

A number of bank customers have since September complained to the CBK that the lenders had imposed arbitrary charges or unilaterally converted their savings accounts into transactional accounts, making them lose the benefits that were accruing from the savings.

On Tuesday, Dr Njoroge insisted banks need to review and scrap all “nuisance fees”, saying such moves have had a significant negative effect on customers.

Banks have recently moved closer to disclosure of total cost of credit with the launch of a new website that shows interest, charges and third party costs on a customer’s loan or mortgage.

PAYE Tax Calculator

Note: The results are not exact but very close to the actual.