Hendrith Vanlon Smith Jr, an American banker, author and Managing Partner of Mayflower-Plymouth Capital LLC, succinctly summarised the centrality of banking in his insightful, “Essays on the Banking Industry,” when he said that “Banks are to the economy what the heart is to the human body.

“They cycle necessary capital through the whole, and they are barely noticed until pressure, necessity or crises.”

The banking system and operations of credit institutions are the lifeblood of any nation’s economic well-being; they are the key turbines of commercial and economic activity.

Banking is among the oldest industries and is believed to have begun around 2000 BC.

In the modern sense of the world, banking can be traced back to the middle ages and early Renaissance Italy, in the affluent cities of Venice, Florence and Genoa.

Locally, the birth of banking dates back to the pre-colonial era. At first, pioneering banks solely focused on facilitating international trade along the Europe-South axis.

They soon diversified operations to tap the opportunities for profitable banking created by a flourishing farming settler community and pioneer merchants to whom they provided banking services.

It was only a matter of time before banking expanded into the hinterland.

The first bank to set foot in the country was Jetha Lila Bankers, but the National Bank of India, which established its first Kenyan branch in 1896, is formally recognised as the first commercial bank.

In the period leading up to independence, Kenya had only three foreign-owned banks: the National Bank of India (NBI), the Standard Bank of South Africa (SBSA), and the National Bank of South Africa, which was later rebranded to Barclays Bank DCO.

Soon after Kenya gained its independence from Britain in 1963, the changing banking landscape witnessed the entry of fully indigenous banks.

The country’s first fully locally owned commercial bank was the Co-operative Bank of Kenya, which started initially as a cooperative society.

It commenced operations in the year 1968 and catered for the needs of growing farming communities.

In the same year, the National Bank of Kenya was founded and became the first financial institution in which the government-owned a 100 percent stake.

In 1971, the Kenya Commercial Bank (KCB) was established following the merger of the National and Grindlays Bank, with the government owning a majority stake of 60 percent.

KCB took pole position as the largest of the country’s commercial banks in terms of deposits and branch network.

From just a handful of banks at independence, Kenya today has 38 commercial banks, more than 1000 bank branches, and upwards of 70,000 bank agents spread throughout the country.

The Kenyan banking industry has evolved tremendously over the last six decades, having experienced many setbacks, successes, innovations, and radical transformations in terms of service delivery and product portfolio, policies, regulatory framework and linkages.

One of the biggest disruptions in banking happened in 1994 when Equity applied for and was granted a licence to operate as a Micro Finance Institution (MFI).

Its strategy premised on a high-volume, low-cost business model upended the prevailing high-margin, low-volume model, and radically revolutionised banking as the hitherto ‘unbankable’ suddenly became bankable.

At a time when other financial institutions were moving out of the rural areas, Equity Bank focused on providing financing to ordinary Kenyans in homesteads, villages and towns.

To lure customers, the bank reduced the entry point to zero and allowed clients to deposit and withdraw money as they wished.

The bank, additionally, slashed ledger and account maintenance fees to a bare minimum.

All this happened at a time when banks imposed minimum deposit requirements for account opening and allowed withdrawals upon prior notice.

Equity bank, thus, reoriented the industry to refocus on those deemed to lie at the “bottom of the pyramid” as its model worked magic in terms of its bottom line.

The drive to reach the unbanked was further given a shot in the arm by the introduction of M-pesa services.

Adopting the Swahili word for money “pesa” and preceded by “M” for mobile, M-pesa was born in Kenya on March 6th, 2007 by the telecommunications giant Vodafone and Safaricom as a phone-based alternative to physical bank branches.

Over time, M-pesa would go on to offer an even wider array of mobile financial services, including virtual savings accounts, loans, and international remittances.

The impact of Safaricom’s flagship product has been phenomenal; it has directly transformed households as it evolved from a basic SIM card-based money transfer application into a fully-fledged financial service, offering loans and savings in partnership with local banks, in addition to merchant payment services.

A Massachusetts Institute of Technology (MIT) research published in 2016 by MIT economist Tavneet Suri, titled “The long-run poverty and gender impacts of mobile money,” found that M-pesa is responsible for lifting 2 percent of Kenyan households out of poverty, which is equivalent to over 250,000 families who no longer live below the poverty threshold on less than $1.00 (Sh135) per day.

In the same year, a part-survey carried out by the Central Bank of Kenya revealed that the proportion of Kenya’s population with access to formal financial services rose sharply to 83 percent from 14 percent back in 2006.

Most banks in the country have integrated mobile banking services into their systems as a means of affording convenience and ease to their customers, hence further deepening financial inclusion.

An amendment to the Kenya Banking Act 2009, which allowed banks to start using agents to deliver financial services was another important milestone in the journey to bolster financial participation.

Under CBK regulations, agents can offer several banking services, including cash deposits and withdrawals, balance enquiry, generation and issuance of mini bank statements, funds transfer, loan repayments, bill payments, and collection of account opening and loan application forms.

A widespread agency network has helped to extend banking services to far-flung and remote rural areas, effectively reaching the unbanked and under-banked population.

Agency banking, together with automated teller machines (ATMs), and online and mobile banking constitute some of the alternative banking channels that banks have leveraged to cut down on costs associated with providing the brick-and-mortar (physical) infrastructure.

Underlining the massive shift to new channels of financial transactions, big banks in the country have reported that over 90 percent of transactions are conducted through alternative banking channels with those done inside banking halls numbering less than 10 per cent.

In efforts to boost cash flow in the economy and lower the cost of doing business, banks in March this year upgraded the Automated Clearing House System (ACH) platform used for electronic funds transfers and cheque clearing.

Following the upgrade, bank customers issued with cheques from rival banks will get value within the same day, a departure from the current trend where they wait for up to two days. Foreign-dominated cheques will clear within two days from seven.

To ensure a delightful and frictionless customer experience in banking halls, banks modernised the queue management system, dropping the physical queueing system, where customers formed snaking lines, especially during peak seasons.

Since banks deal in money, they have often been a target of criminals eager to live at rack and manger. Over the past few years, the number of reported bank robberies has drastically reduced owing to increased security in terms of surveillance and armed police officers manning banking facilities.

In the late 90s and early to mid-2000s, bank robberies were common with millions of shillings being reported missing.

The 1999 Mashreq bank heist will go down in history as perhaps one of the most daring and hilarious heists in the country.

In July 1999, a group of armed robbers invaded the bank then situated at the ICEA building along Kenyatta Avenue and casually walked away with Sh500,000, which was a tidy sum back then.

What made it so amusing was that the robbers were so comfortable that they sang a popular tithing song, “Toa ndugu, toa dada ulichonacho wewe,” as they robbed the bank’s customers.

In yet another bold heist, a group of men disguised as auditors walked into Equity Bank’s Othaya branch and fled away with cash estimated at Sh50 million.

Media accounts of the theft indicated that the robbers walked into the branch and were ushered in by the operations manager, but shortly after pulled out knives and demanded to be shown the vault where they stole the cash.

However, today’s criminals are not gun-toting, macho men with identities masked behind sunglasses and balaclavas out to instil terror while demanding instant surrender, but computer geeks keen to exploit loopholes in banking systems to hack and manipulate money transfers.

Though considered the most mature, fastest-growing and largest in East Africa, the banking industry has, however, been a victim of both global and domestic financial challenges.

The country’s financial industry in the past three decades has been characterised by major financial upheavals that resulted in the collapse of several banks, while others were in and out of receivership.

The crises were mainly attributed to a high amount of non-performing loans, anaemic internal control mechanisms, political interference, weak governance structures and subpar leadership.

Some of the banks that have collapsed in the recent past include Imperial Bank, Dubai Bank, Charter House Bank and Chase Bank among others.

Overall, the Kenyan banking sector has performed efficiently over time, thereby contributing significantly towards driving and shaping the country’s GDP growth.

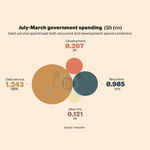

Key contributions are in job creation, wealth creation, taxes and credit access. The government, for instance, in the 2016/17 – 2017/18 financial years collected more than Sh143 billion as taxes from the banking sector, which was the single biggest contribution by any industry to the taxman’s coffers.

Moreover, Kenyan banks lent out a cumulative Sh480 billion to the National Treasury over three years (2016-2018) – funds used to spur development and meet the government’s recurrent expenditure.

For banks to continue thriving as going concerns, they must institute robust internal control mechanisms capable of detecting and weeding out financial malpractices, which might ruin them.

Banks must equally eschew excessive risk-taking like in the US case, where Silicon Valley Bank collapsed due to injudicious risk management.

Banks must also ensure full compliance with existing Anti-money laundering and counter-terrorist financing (AML/CFT) regulations to guard against penalties and reputational harm.

What are some of the lessons that we can draw from advanced economies? Canadian banks have long been a byword for stability.

The country has had only two small regional bank failures in a century and had zero failures during the great depression of the 1930s.

How did Canada achieve that impressive result in an era characterised by dramatic bank failures?

Firstly, the diversification and adoption of the “universal bank” model. The existence of a large branch network and strong brand equity has provided all Canadian banks with stable retail and commercial deposits and a corresponding healthy loan-to-deposit ratio.

Core deposits are well diversified geographically- as are the loans, which are spread not only across all the regions but also among different industry sectors and consumers to diversify the risk.

The universal bank model also encourages a customer-centric approach to business.

Secondly, Canadian banks have benefitted greatly from efficient management practices which is the hallmark of any successful financial system.

All Canadian banks have an enviable loan loss performance which can be attributed to sound management of credit risk at the transaction level, and experienced, tenured and highly qualified lenders on the front line.

Thirdly, Canada’s regulatory and supervisory framework has performed exceptionally well.

The authorities are much more conservative regarding capital levels and set high requirements to protect the banking system from economic shocks.

In fact, Canada is home to some of the best-capitalised banks in the world.