Time flies with great content! Renew in to keep enjoying all our premium content.

Prime

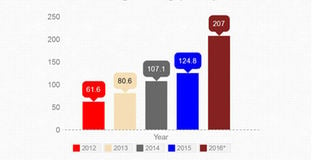

Borrowers hit hard times as bad loans rise to Sh207 billion

Central Bank of Kenya building. The regulator has also lately enforced more stringent rules in accounting for bad debts following the collapse of three banks in quick succession. PHOTO | FILE

The stock of bad loans held by commercial banks has crossed the Sh200 billion mark for the first time ever, betraying hard economic times facing Kenyan households and businesses as well as more stringent accounting standards set by the regulator.

Third-quarter bank announcements show the value of bad loans shot by Sh17 billion in the three months between June and September as businesses and households lagged behind their debt payment schedules.

This raised the total non-performing loans book to Sh207 billion, appearing to discount overall gross domestic product (GDP) growth figures, which have ranged above five per cent in recent years.

Deep job cuts by companies struggling to cushion their profit margins have left many households with the grim choice of either honouring loan repayments from diminished income or defaulting on their obligations to meet basic needs.

The drop in household incomes has hit people’s spending power, in turn shrinking the overall demand for goods and services.

“The increase in gross non-performing loans was mainly attributable to challenges in the business environment that led to cash flow constraints for borrowers,” says the Central Bank of Kenya (CBK) in its Credit Survey Report dated September this year.

GRAPHIC | LYNETTE MUKAMI

The regulator has also lately enforced more stringent rules in accounting for bad debts following the collapse of three banks in quick succession.

The defaults mean that 9.1 per cent of the Sh2.28 trillion loans issued by banks have not been serviced in the past three months, an increase from the 8.4 per cent default rate reported by banks in June.

The piling load of non-performing loans puts in focus reported GDP growth figures-- 5.9 per cent for the six months to June-- and whether the growth is trickling down to businesses and households.

The Kenya Revenue Authority has successively missed the annual tax targets set by the Treasury citing a sluggish job market and lower corporate taxes.

Banks have previously attributed the defaults to delayed payment of contractors’ bills by the government. The Treasury has lately accelerated release of money to the contractors, but bad loans have continued piling.

“Most of the banks have been saying it is a few large borrowers but you have to ask how much have these borrowers borrowed and how come it is these few borrowers every quarter?” asked the head of research at Standard Investment Bank, Francis Mwangi.

Banks are expected to be more aggressive in their efforts to recover the dud loans, with industry sources telling the Business Daily that bank managers were pushing most of the bad borrowers to auctioneers in a bid to improve their books before year end.

Small businesses and low-income households are usually forced to sell their assets to pay debts, according to a study this year by not-for-profit organisation FSD Kenya.

FSD found that more than a quarter or 28 per cent of households categorised as poor had sold an asset in the past year to pay a debt while the wealthy had been refinanced by banks.

Banks are expected to hold back on issuing new loans as they race to clean up their books first.

“In Kenya’s banking history credit growth has been more sensitive to non-performing loans than interest rates, as it pushes banks to be more conservative,” said Mr Mwangi, adding that banks would keep a tight purse in spite of recent interest rate reduction.

Loan approvals have gone up at a slower pace (4.7 per cent) than the rate of application (14.8 per cent), the CBK said last week, underlining credit rationing by banks.

Borrowing has slowed down to its lowest level in more than a decade, with industry data showing lending grew by 4.8 per cent in the year to September compared to 20.6 per cent in a similar period last year.

Lending to traders and manufacturers has reduced over the same period, indicating that investors are not seeing new funding opportunities in the economy.

Most banks, especially the medium and small-sized lenders, have low cash levels as indicated by their liquidity ratio due to the cash crunch in the economy and flight to safety by depositors following the recent collapse of three banks. The rise in defaults has also been attributed to stricter enforcement of regulatory requirements on non-performing loans by the CBK following a change of guard early last year.

Commercial banks have for long fought accusations of inflating their profitability by understating their non-performing loans.

Understating of bad loans allows banks to set aside lower provisions for defaults, a deductible expense in their profit and loss accounts.

Under-provisioning for bad loans may help banks report better profits, but in the event that a large number of borrowers default it exposes them to financial difficulties and even possible collapse.

Bad loans are a danger to the banking sector and have previously been blamed for the collapse of some lenders.

Seven large banks in the country are carrying Sh90.5 billion of the bad loans, equivalent to 44 per cent of the industry total.

Standard Chartered has the largest default rate among the large lenders at 12 per cent followed by Commercial Bank of Africa and KCB.

Lenders with huge piles of non-performing loans include National Bank (47 per cent of its loan book) and Shariah-compliant First Community Bank at 25 per cent.

Credit officers surveyed by the CBK said they expected the stock of dud loans to remain unchanged.

Non-performing loans eat into the returns of bank owners, as seen in the industry return on equity decline to 27 per cent in September from 33.8 per cent in June.

Unlock a world of exclusive content today!Unlock a world of exclusive content today!