Time flies with great content! Renew in to keep enjoying all our premium content.

Prime

Tatu City feels the weight of debt after shareholder wars

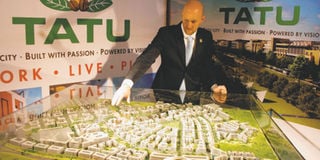

Former acting Tatu City CEO Arnold Meyer (left) explains the project’s concept to a journalist. FILE

One of the top shareholders in Kenya’s largest real estate development project, Tatu City, has exited, slowing down its execution plan.

Stephen Jennings, the founder and long-serving CEO of Renaissance Group – the company that owns Tatu City – stepped down early this year after spinning off the profitable businesses in the group.

People familiar with the matter said Renaissance is also experiencing a cash crunch and is struggling to restructure a $272 million (Sh23 billion) debt that has seen it opt to sell or rethink its large-scale real estate developments in Africa.

“The challenges facing the group cannot be overestimated and the threat of insolvency remains ever present,” Hans Jochum Horn, a director of Renaissance Holdings, told creditors in a letter dated February 6, 2013.

Renaissance in April completed the sale of its remaining 50 per cent stake in investment bank Renaissance Capital to Onexim group, which is owned by Russian billionaire Mikhail Prokhorov.

Onexim also simultaneously took a controlling 89 per cent stake in Renaissance Credit that was until then part of Renaissance Group. The twin transactions have seen Renaissance reverse from a diversified holding company to essentially an owner of land parcels in several African countries.

The company is now weighing the option of developing the land in smaller phases or selling altogether to stay liquid. A preliminary action plan specific to Tatu City shows that Renaissance Group has decided to “rationalise the platform,” signalling a potential reduction of the project size.

The company insists that its priority now is to stay liquid and that it will dispose of fixed assets that don’t generate any cash, further casting doubt on Tatu City’s prospects.

“I have demanded that each asset provides liquidity for the group or it is disposed of,” the letter reads further. “The group is working to restructure its debt and to rationalise its operating assets.”

Renaissance plans to raise a total of $40.5 million (Sh3.4 billion) from the sale of its land holdings in Zimbabwe, Ghana as well as the disposal of other business lines such as its asset management business. Tatu City is listed as Renaissance’s most valuable asset at $130 million (Sh11 billion).

Court documents show that Renaissance had arranged a $62.5 million (Sh5.3 billion) loan from international lenders to partly fund the Tatu City project, but it is unclear whether the debt is part of the $272 million it is asking creditors to restructure.

Tatu City was pitched as Kenya’s largest planned urban development that was to be executed by private investors. The multi-billion- shilling development was to host 25,000 houses and 62,000 people on a 2,400-acre land in Kiambu.

Tatu City executives, however, remain upbeat that the project will be completed as advertised despite the new challenges that have only exacerbated the three-year shareholder wars.

“Tatu City is definitely on,” said Lucas Omariba, the chief executive of Tatu City Limited, adding that Renaissance and other local shareholders, including businessman Vimal Shah and former Central Bank governor Nahashon Nyaga, remain committed to its full implementation.

Mr Omariba said the shareholders own the land outright and that financing of the development will be sourced from the shareholders and local banks.

The firm is to sell plots to individual and institutional investors who are expected to build homes and other properties according to approved designs. It remains to be seen whether Tatu City will weather the shareholder disputes and the cash crunch facing Renaissance, the main force behind the project.

Mr Omariba said that most of the prayers sought by minority shareholders Stephen Mwagiru and his mother, Rosemary Mwagiru, have been dismissed by the courts, allowing Tatu City to start selling plots and developing the land.

The Mwagirus, who are believed to own the land on which Tatu City is to be built, claim that they have been sidelined in the management of the project estimated to be worth more than Sh100 billion.

The courts have thrown out the Mwagirus’ bid to have Tatu City wound up and have also dismissed the litigants’ application to bar the company from selling any of its plots. Mr Omariba, however, said that the Mwagirus have filed a notice to appeal the court decisions, implying a protracted legal battle.

Barring any new injunctions, Tatu City is ready to start selling plots to interested buyers ahead of breaking ground on the first residential phase early next year.

Mr Omariba said earthworks (land preparation) for this phase have been completed by SS Mehta and Sons, the contractor hired last year for Sh300 million.

Tatu City is set to issue a tender for civil works, including the laying of electricity and infrastructure for the same phase.

The project’s success, however, depends on the ability of its promoters to win back the confidence of the investing public and financiers, including local lenders and creditors of Renaissance who have been asked to extend the tenure of their loans.

“All creditors are faced with the same set of facts. Namely, that the best chance of realising value will at least involve extending maturity dates,” Renaissance told its bondholders in the letter.

It remains unclear what Renaissance means by “rationalising” Tatu City.

The statement is seen by some as expressing the expectation that the development may not match its earlier grand plans.

The court cases have seen the project delay by nearly four years putting the company in a high executive turnover mode. Scores of the company’s employees have also been sent home.

Tatu City’s acting CEO Arnold Meyer quit in February this year, with the firm’s chief financial officer (CFO) Craig Young also leaving in August.

Unlock a world of exclusive content today!Unlock a world of exclusive content today!