Kenyan borrowers have now defaulted on more than Sh596 billion in loans as rising interest rates wreak havoc on the country’s banking sector loan book, setting up more households and businesses for a fresh round of auctions and property seizures as lenders move to recover bad loans.

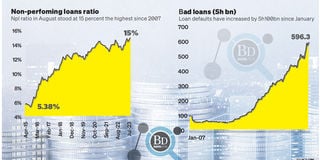

Latest data from the Central Bank of Kenya (CBK) show that the stock of non-performing loans (NPLs) in Kenya surged to a 16-year high of 15 percent in August, up from 14.5 percent in July. This translates to more than Sh596 billion, worked as a share of the total loan book.

The CBK data show that the increase in loan defaults has been observed in manufacturing, mining and quarrying, real estate and building and construction.

The loan default rate matches up to the NPL ratio of 15.4 percent that was posted 16 years ago in June 2007.

The rise in the bad loans has been attributed to rising interest rates on commercial bank loans which have weighed heavily on customers servicing the facilities amidst a deteriorating macro-economic environment.

“The rise in interest rates has primarily come from decisions taken by the Monetary Policy Committee to stabilise the economy but have meanwhile resulted in pain in the short run,” Kenya Bankers Association (KBA) CEO Habil Olaka told the Business Daily in an interview last week.

“When rates go up, demand for credit goes down but even the existing portfolio starts having challenges.”

Waning demand

According to the banking sector lobby, the ability of businesses to service loans has been affected by waning demand from consumers as Kenyans contend with a high cost of living.

Equally, businesses have faced increased costs of production from elevated input prices, including the cost of electricity.

The deterioration in the banking sector asset quality could see commercial banks decrease their issuance of new loans as a way of containing the rising NPLs.

Banks could resort to measures mimicking those induced by the Covid-19 crisis to stabilise their loan books, including extending repayment periods to customers.

“Banks have been focusing less on building up their portfolio and focusing more on containing their portfolio. It means working with the clients, not necessarily in terms of collections but managing borrowers through the turbulence, ensuring loan facilities do not advance from doubtful to loss. Otherwise, one may take actions that might ‘kill’ the customers, if say you throw auctioneers at them- the customer may not recover,” added Mr Olaka.

At the onset of the Covid-19 pandemic, the CBK directed banks to provide relief to borrowers whose loans were up to date, based on their individual circumstances arising from the pandemic.

The lenders were allowed to request for the extension of their loan repayment periods by up to one year.

During the period, the CBK took an accommodative policy stance by also lowering its benchmark lending rate, the Central Bank Rate (CBR), and the banks’ cash reserve ratio, which remains at 4.25 percent at present.

Recent months have nevertheless dictated that the apex bank tightens monetary policy, with the CBR rising to a near seven-year high of 10.5 percent in June.

The increase has primarily set off the subsequent lift-off to commercial banking interest rates alongside yields on other interest-bearing assets such as government securities.

Average commercial bank lending rates have risen to a 65-month high of 13.5 percent as of July while yields on short-dated Treasury bills hit 15 percent as of last week with respect to the 364-day paper.

The higher interest rates are nevertheless yet to dampen the demand for credit, with private sector credit growth recovering to 12.6 percent in August from 10.3 percent in July.

Strong credit demand has been observed in manufacturing, transport and communication, trade and consumer durables.

“The number of loan applications and approvals remained strong, reflecting resilient economic activities,” the CBK said on Tuesday.

The CBK noted the effects of the last jumbo-rate increase in June was still being transmitted in the economy, informing its decision to retain the CBR at 10.5 percent.

“The MPC noted that inflation is expected to remain within the target range, supported by lower food prices with the expected improved supply. Additionally, the MPC observed that non-food non-fuel inflation was expected to decline, indicative of easing underlying inflationary pressures,” the CBK added.

The CBK had been widely expected to hold the benchmark interest rate on easing cost of living, with inflation having reset down to the CBK’s target band at 6.8 percent in September.

Concerns on rebounding inflationary pressures have, however, been noted from the continued spike in both global and domestic fuel prices.

Despite the rise the NPLs, the CBK notes the sector remains stable and resilient, with strong liquidity and capital adequacy ratios.