Time flies with great content! Renew in to keep enjoying all our premium content.

Prime

Merali’s swift exit from Zain earns him billions

Naushad Merali reaps Sh4 billion from sale of 15 per cent shareholding just in time before a revaluation impairs it. Photo/ANTHONY OMUYA

Businessman Naushad Merali’s decision to significantly reduce his stake in telecoms firm Zain Kenya last year was yet another of the many sumptuous investment hat tricks he has pulled among local and foreign business partners in the past 10 years, it has now emerged.

Shortly after Mr Merali’s stealth exit, Zain Kenya, the telecoms service provider which is now 95 per cent owned by Kuwait-based Zain Group, became the subject of a major asset impairment that cut back the firm’s valuation by more than Sh5 billion.

In its latest consolidated financial statements, Zain Group reveals that Mr Merali, who is the firm’s sole local shareholder, earned ($63.75 million) or Sh4 billion from the 15 per cent stake he sold – leaving him with a five per cent claim in the operation.

Zain Group says that shortly thereafter, it had to subject the Kenyan operation to an impairment charge because its working capital was in deficit during the last financial year.

Reginald Kadzutu, the head of Fund Management at Amana Capital, reckons that an impairment charge is typically imposed on a business when its book value has front run the fair value.

This is usually determined by a number of factors, including net cash flow expected during a specified operation period.

“An asset is considered to be value-impaired when its book value exceeds the future net cash flows expected to be received from its use,” said Mr Kadzutu.

The impairment is therefore a write-down on a company’s book value that effectively reduces the overstated value to a fair value.

“When the book value or original cost of assets becomes higher than the market value, and it is reported the fair value or market value is actually less, then its value (which is another reference to its viability) gets impaired heralding a correction,” said Mr Kadzutu.

In Zain Kenya’s case, the write-down was worth Sh6 billion in what the parent firm attributes to a huge working capital deficit in the last financial year.

That deficit has been blamed on the vicious dog-fight that Zain Kenya has had to undertake in the past couple of years using tariff cuts as the main weapon.

In its latest earnings report, Zain said it had executed the impairment charge ahead of the sale of the company to India’s Bharti Airtel in a $9 billion deal concluded recently.

Analysts said increased competition and a worsening of economic conditions in Kenya in the past two years that produced lower than anticipated revenues were the main drivers for the impairment charge.

Although industry regulator, the Communications Commission of Kenya (CCK), says that the average revenue per user (ARPUs) in the country fell during the past year, the mobile telephone market grew by 13 per cent.

Zain Kenya recorded an all-time ARPU low of $4 in 2009, down from $7 during the same period in 2008.

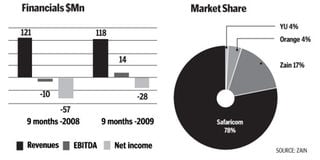

The company recorded a reduced loss in the nine months to September 2009 at $25 million (Sh1.8 billion) compared to a loss of $57 million (Sh4.2 billion) in the same period a year earlier.

Its revenues, however, declined from $121 million (Sh9. billion) to $118 (Sh8.8 billion) in the period under review—a clear signal that the lower losses were driven by cost cutting measures.

Competitive forces also saw the new entrant Telkom Kenya record a Sh10 billion loss in 2009.

Market leader Safaricom’s profits for the six months to September 2009 grew 1.7 per cent to Sh9.1 billion from Sh8.9 billion.

Analysts at Renaissance Capital attributed the steep drop in Zain’s ARPUs to market forces that spawned a debilitating price war in 2008 and early 2009.

That war saw Zain over-stretch itself on the tariff front, introducing significantly lower calling costs whose impact was to attract lower spending subscribers that ultimately hurt its profit margins.

Plotted the sale

It is against these market movements that Mr Merali quietly plotted the sale of 15 per cent of his stake in the company.

Had Mr Merali delayed his decision to sell the 15 per cent, the impairment would have greatly reduced the value of his stake in the telecoms firm and significantly reduced his take home upon exit.

Zain Group says that while the various valuation approaches showed a variety of outcomes, the management decided to impose an impairment charge of Sh6 billion on Zain Kenya based on the lower end of the range of valuations obtained.

Mr Merali’s decision to sell 15 per cent of the 20 per cent share he held in Zain Kenya was the latest in a series of calculated moves that have seen him gradually reduce his shareholding in the operation he launched as KenCell 10 years ago.

The methodical exit plan staged over the past four years, started soon after the 2004 boardroom coup that saw him engineer an exceptionally lucrative sale of KenCell to Celtel.

That plan has helped him to whittle down his stake in the telecoms firm from the original 40 per cent to five per cent with each move coming at strategic points in the firm’s history.

Sameer Group, Mr Merali’s investment company, jointly launched KenCell Communications with its French partner Vivendi in 2000.

But three years later, when the French firm decided it was time to leave Kenya, Mr Merali used his pre-emption rights to stage one of the smartest boardroom chess games that played a number of global telecoms giants against each other for Vivendi’s stake.

He ultimately sold the stake in 2004 at a sumptuous $250 million and at the same time started the journey out of the company with the sale of 20 per cent of his 40 per cent stake to the new partner Celtel International.

At the time MTC bought Celtel out of 16 African countries in 2005, Merali’s stake stood at 40 per cent.

In 2008, He sold half of it to Zain and further reduced it to five per cent with the 15 per cent sale last year.

Zain has since sold its stake to India’s Barti Airtel who are now Mr Merali’s only partners in the business.

Mr Merali’s exit from Zain triggered an industry-wide revisit of local share holding rules previously imposed by CCK.

When the sector was first liberalised at the turn of the millennium, foreign ownership of Kenyan telecoms firms was capped at 20 per cent leaving locals with an 80 per cent stake.

This regulation has however been gradually revised over the years to create room for more foreign ownership – a move that the state says has helped attract direct foreign investment into the economy.

By last year when Mr Merali sold part of his stake in Zain Kenya, the cap on foreign ownership had moved up to 80 per cent, rolling back the requirement for local ownership to a mere 20 per cent.

Unlock a world of exclusive content today!Unlock a world of exclusive content today!