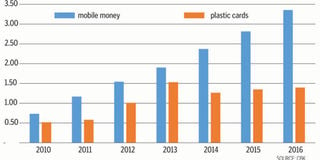

Payments made using plastic cards slowed down further last year as the gap between mobile money and swiping to settle bills continues to widen, driven by convenience of phone-based cash.

Card payments posted a sluggish 3.6 per cent growth to Sh1.39 trillion in 2016, slower than the 6.6 per cent jump registered a year earlier, according to latest data from the Central Bank of Kenya (CBK).

They trailed behind mobile payment volumes which grew by a fifth last year to hit Sh3.35 trillion, continuing a double-digit growth trend over the last decade.

Naivas Supermarkets chief commercial officer Willy Kimani said mobile payments have doubled to 11 per cent from five per cent of total sales last year at the retailer, adding that the segment continues to grow.

Experts argue that the continued dominance of mobile money payments in Kenya over plastic cards is attributed to convenience, safety, cost, availability of infrastructure, and the shorter settlement cycle offered by mobile cash.

“It’s about convenience. Mobile cash paybill numbers are now available even in nyama choma joints, groceries, and even in the villages,” Dr Peter Muriu, a lecturer at the School of Economics, University of Nairobi, told the Business Daily.

“There are also safety concerns. Whenever you make a mobile money transfer, you can easily verify the balance. In the past there have been instances in which if you swipe card while making payments, cash is deducted twice.”

There were 14.8 million payment cards in use, compared to 34.9 mobile money subscriptions as at December 2016, according to the CBK.

The decline in card payment volumes comes at a time when Kenyan banks have begun piloting their own mobile money platform dubbed PesaLink, seeking a slice of the lucrative phone-based payments market.

Banks hatched the plan to establish a mobile phone-based direct money transfer system in 2012 in the heat of financial pressure from services such as M-Pesa and MobiKash, which they argue were eating into their transaction fees revenue.

Michael Kimani, an e-payments analyst, reckons that setting up a mobile money paybill is easier than card payment set up which requires a bank account, point-of-sale machine, and a processing fee.

“Setting up a mobile till number is a low cost affair. Besides, merchants at times use their personal mobile money accounts as business accounts,” said Mr Kimani, co-founder of bitcoin firm Umati Blockchain.

“There are more people in Kenya with mobile phones than cards.”

Kenya’s total number of point of sale terminals stands at 30,133 and is seen as the missing link in getting more Kenyans to adopt card payments.

This translates to a per capita ratio of one card payment terminal for every 1,500 Kenyans.

On the flipside, the number of traders accepting mobile money payments in Kenya is estimated at more than 100,000 — offering consumers more touch points to pay via mobile cash than using plastic cards. The number of active Lipa na M-Pesa outlets has doubled in as many years to more than 50,000 merchants as at end of last September, made up of supermarkets, fuel stations and hotels among others.