Bank owners’ return on investment low after capital injection

KCB investors go through published financial results during a past annual general meeting. PHOTO | FILE

What you need to know:

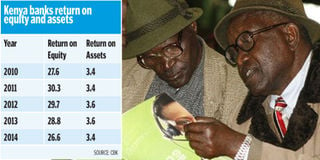

Data from the Central Bank of Kenya (CBK) shows that the bank posted a return on equity (ROE) of 26.6 per cent lower than the previous year’s 28.8 per cent despite a 13.3 per cent jump in pre-tax profits.

However, the Kenya banks’ ROE is much higher than in, say, the United States where stress tests on 31 banks recently revealed that they have an average ROE of eight per cent.

ROE calculates how much profit a company generates with each shilling of shareholders’ funds while ROA shows the profit that a company earns in relation to the overall wealth that it has created from its business such as loans.

Bank owners received a lower return for their investment in 2014 compared to the previous year following increased capital injections.

Data from the Central Bank of Kenya (CBK) shows that the bank posted a return on equity (ROE) of 26.6 per cent lower than the previous year’s 28.8 per cent despite a 13.3 per cent jump in pre-tax profits. The increase in capital depressed the relative returns both on equity as well as on assets.

“The annualised return on assets (ROA) declined to 3.4 per cent from 3.6 per cent over the same period in 2013. Similarly, ROE decreased to 26.6 per cent from 28.8 per cent over the same period,” said CBK in a newly released report.

However, the Kenya banks’ ROE is much higher than in, say, the United States where stress tests on 31 banks recently revealed that they have an average ROE of eight per cent. European banks also had a ROE of 4.6 per cent in the first half of last year, according to data from the European Central Bank.

The industry’s total profits before tax increased by 13.4 per cent to Sh140.9 billion last year from Sh124.3 billion riding on increased lending at a time of high interest rates.

Shareholders were forced to inject additional capital in the industry to support the growing businesses and comply with higher statutory capital requirements that came into effect at the beginning of this year.

“Banks increased capital significantly last year so you expect the return to drop but they are not any less attractive to investors – the profits are still high,” said Ashif Kassam chief executive of audit firm RSM Ashvir.

ROE calculates how much profit a company generates with each shilling of shareholders’ funds while ROA shows the profit that a company earns in relation to the overall wealth that it has created from its business such as loans.

Some of the lenders that raised additional capital from shareholders include DTB, NIC, Chase Bank and Commercial Bank of Africa. The firms raised cash through rights issues.

Central bank said banks’ core capital, which is shareholders funds, increased to Sh422 billion in December from Sh342 billion a year earlier.

The bank’s total assets increased by 19.3 per cent to Sh3.2 trillion from Sh2.7 billion with loans being the main component at 58.3 per cent followed by government securities at 20.4 per cent.

Kenyan banks have been ranked tops in offering best returns to shareholders and in squeezing their assets for optimum gain in the last two years.

The high returns have been a major attraction to investors who have flocked to banking counters on the Nairobi Securities Exchange or purchased equity as strategic investors in private banks.

A survey on 1,000 largest banks globally done by The Banker, a publication of the London-based Financial Times, showed Equity Bank had the highest ROA in Africa and the third globally while KCB ranked third in the continent.

Equity had a return on asset of 6.84 per cent while KCB achieved a return on assets of 5.14 per cent. Bank customers have however pointed at the returns as indication of room for lowering of transactional costs and lending rates.

“The comparison (in return on assets and on equity) implies that there is room for Kenyan banks to lower their charges as a way of sharing efficiency resulting from the various reforms and innovations rolled out by the players,” said a committee formed by the government to interrogate the high cost of lending in a report released last year.

Banks are allowed to contract agents to offer some limited cash-based banking services such as depositing and withdrawing of money. Use of agents, who must be operating existing businesses such as retail outlets, has allowed banks to increase their out reach without incurring the costs of setting up branches.

The bankers have however defended their margins by arguing that their shareholders are taking high risk with their money given most of the borrowers are small-scale businessmen.

PAYE Tax Calculator

Note: The results are not exact but very close to the actual.