Four months to the 2017 General Election and real estate, like other sectors, is both excited and nervous about the post poll period.

The economy takes a dip every election cycle as political campaigns take centre stage and businesses hold back on investments to await the outcome of the polls.

The Central Bank of Kenya has projected that the economy will grow by 5.7 per cent this year, slowing down from 5.9 per cent in 2016.

The International Monetary Fund and the World Bank have also projected a sub-six per cent growth rate.

Real estate players HassConsult, Cytonn Investments and Knight Frank have, however, remained bullish on the sector, which has witnessed fast growth in recent years.

HassConsult said investors are likely to adopt a wait-and-see stance in the run up to the elections, with a price fall in the sector unlikely even if the number of transactions reduce.

“We have not seen a drop in prices as a result of impending elections, instead we expect to see a flattening in price increases which actually lends the property market more stable price growth,” HassConsult research and marketing manager Sakina Hassanali told the Business Daily.

Ms Hassanali said the upcoming elections have so far not affected long-term investments in the real estate sector.

“Long term investments in the real estate sector do not fluctuate around elections given that projects have a long term horizon and return projections,” she said.

Cytonn Investment said the real estate sector is likely to remain bullish, assisted by election spending.

“Increased liquidity is a recipe for increased investment in the real estate sector and hence leads to an increase in property value. This has a positive effect on the real estate sector,” said Cytonn in a recent bulletin.

The firm added that its positive outlook for real estate was informed by “demographics, high demand for real estate products — especially housing units — and increased infrastructure development.”

House prices rose at a slower rate in the final quarter of 2016 compared to the preceding period due to an economic slowdown and a decline in sales in the wake of poor credit uptake.

The Kenya Bankers Association (KBA) housing price index shows house prices rose by 1.58 per cent compared to the third quarter’s 2.2 per cent.

KBA chief executive officer Habil Olaka linked the trend to “traces of the effect of the rate capping law.”

The bankers’ lobby is fiercely opposed to the Banking (Amendment) Act 2016 which introduced legal caps on interest rates and came into force on September 14, 2016. Some analysts had predicted that the law would trigger increased uptake of mortgages.

“The number of housing units whose sale was concluded during the quarter were lower than those of the previous quarters,” said Mr Olaka.

According to Jared Osoro, the director of research and policy at KBA, the mild price increase — albeit at a slower rate than in the previous quarter — could be directly linked to the rate control.

“Whereas the general trend in house prices has been positive, the mild dipping during the fourth quarter was a reflection of market adjustment in response to the new dispensation on the back of the new banking law,” he said.

Mr Osoro, however, noted that house prices have increased by 14.91 per cent since the first quarter of 2013, the base period for the KBA house price index.

However, KBA projects a spike in construction sector activity.

“We expect a surge in residential construction activity as the financial sector adjusts to the new pricing regime,” said Mr Olaka.

“Our anticipation is that a number of facilities that were pending approval will have been completed and developers will seek to bring to the market ongoing housing projects.”

The Cytonn report said that apartments accounted for about 60 per cent of units sold during the quarter compared to 23 per cent and 17 per cent for maisonettes and bungalows respectively.

“Apartments have a shared sense of communal housing and this has proved a preference for the urban middle class.

‘‘They also have amenities like malls which are seen to be prioritised by the middle class,” said Mr Osoro.

Core housing attributes influencing buyer demand, according to the report, are size of the house, the number of bedrooms and how large they are, bathrooms, presence of detached servant quarters, parking space and availability of water.

The report said that developers are keen to continue supplying the middle and high-end housing markets which have higher returns.

“Evidently the market reflected dominance of activity of the middle and upper end than the lower end as supply remained aligned to that segment,” said the report.

A survey by real estate firm Hass Consult shows that the recent capping of interest rates has failed to trigger an uptake of mortgages and ownership of land.

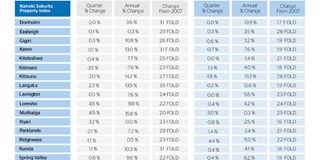

Hass Consult’s Hassanali said the asking price for land in Nairobi rose by a marginal 0.8 per cent in the fourth quarter of last year and 5.1 per cent year-on-year.

On the other hand, property prices in Nairobi suburbs increased by a marginal 0.1 per cent in the same period and posted a 7.6 per cent return over the year.

The rate marks the lowest growth rate for Nairobi’s property market in eight years and comes amid a bank credit squeeze.

“The subdued performance can be attributed to the slow growth in credit as a result of the interest rate cap law which has failed to live up to market expectations,” said Ms Hassanali when the firm released its 2016 quarter four property and Nairobi land price index.

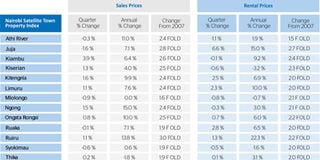

The index includes quarterly changes in asking and letting prices in Nairobi’s 18 suburbs and 14 satellite towns.

“In the last quarter, the market was optimistic that the interest rate cap law would result in advancing more affordable credit that was expected to increase loan uptake and spur the property market. Unfortunately, this has not been witnessed as banks are more cautious in lending,” added Ms Hassanali.

The Banking (Amendment) Act 2016 sets the maximum lending rate at four percentage points above the Central Bank Rate (CBR).

The law also sets minimum returns payable by banks on customer deposits at 70 per cent of the CBR.

The CBR is currently set at 10 per cent, meaning that banks are barred from charging interest on loans above 14 per cent.

Financial institutions offered mortgages at between 12 and 21.4 per cent before the rate cap.

The public was told that the low rates were beneficial to Kenyans out to own homes.

Analysts argued that the rate was likely to incentivise potential home buyers, most of who had been locked out of the mortgage market.

“Accessibility and affordability of mortgages will become a reality now. More people have been netted into the basket of being able to borrow or take up a mortgage in the banking sector.

‘‘This is a big development for the housing and construction industry,” Britam Asset Managers chief investment officer Elizabeth Irungu said.

Unlock a world of exclusive content today!Unlock a world of exclusive content today!