Regional markets have proved a tough nut to crack for Kenyan banks despite ambitious expansion drives, a new report shows.

The restive South Sudanese market has particularly been unpleasant for Kenyan lenders—killing ambitions of tapping opportunities in the newest member of the East African Community (EAC) bloc.

An analysis of bank operations done by global investment bank Renaissance Capital (Rencap) shows that the returns from regional subsidiaries for Kenyan banks have fallen to less than half of their Kenyan operations.

As such, Rencap says, lenders such as KCB, Equity and Cooperative banks, which have invested significantly to establish a regional footprint may have to rethink their approach in these markets.

“We conclude that despite restricting expansion to the East Africa, the Kenyan banks have struggled to make waves in these markets… in our view, ramping up profitability in the various subsidiaries should be the key focus of management,” says Rencap in their Africa banks sector update for February.

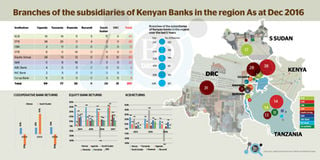

These lenders have been forced to close down tens of branches in South Sudan, a market that was promising to be most lucrative for them due to the relatively low development of the banking sector and linkages of local businesses to Kenya.

In the other markets, while there has been some growth, the return on assets has remained well below the growth of the asset base.

The Rencap analysis shows that KCB, which has operations in Tanzania, Uganda, Rwanda, Burundi and South Sudan, was only able to derive a double digit return on equity in Kenya and Rwanda in 2016 at 17 and 14 per cent respectively, with Tanzania (nine per cent), Uganda (five per cent), Burundi (three per cent) and South Sudan (-26 per cent) all trailing far below.

“We believe that South Sudan will continue to struggle in the short-to-medium term, in light of the economic challenges. South Sudan is experiencing hyperinflation, and as long as KCB continues to operate in such an environment, costs will continue to be a considerable challenge,” says Rencap.

For Equity Bank, operations in Uganda, South Sudan, Rwanda, Tanzania and DR Congo brought a return on equity of 18 per cent in the first nine months of 2017, compared to the Kenyan unit’s return of 38 per cent.

The bank, Rencap says, was more proactive in reducing its footprint in South Sudan at the onset of civil unrest, and was thus able to avoid the cost pitfalls that have hit KCB.

Co-operative Bank’s only regional operation is in South Sudan, where the returns went from 97 per cent in 2015 to -50 per cent in 2016, while in Kenya its return was at 34 per cent in 2016.

Unlock a world of exclusive content today!Unlock a world of exclusive content today!