Airtime has become a top consumer of the highly popular digital loans in Kenya, a new survey confirmed, beating other household necessities such as a medical emergency.

A Central Bank of Kenya (CBK) financial stability report shows that airtime took up 15 per cent of digital loans, only trailing business (37 per cent), day-to-day needs (25 per cent) and education (20 per cent).

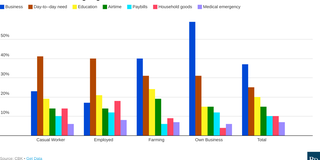

The uptake loans for airtime is highest among farmers, according to the report, while both casual and permanently employed workers tied in the pace of accessing this type of credit.

The findings back a previous World Bank study in 2013, which showed that many of Kenya’s poor would rather go hungry and walk to work than be short of airtime.

The study found that seven out of 10 poor people — referred to as the base of the pyramid in the report — cut down on food expenses to spare money for airtime.

Digital credit has expanded drastically in Kenya since adoption in 2015 as financial institutions seek ways of expanding financial access.

For example, the FinAccess Digital Credit Tracker 2017 shows that 26 per cent of Kenyans are digital borrowers, with more than 20 digital credit providers operational in Kenya, including M-Shwari, KCB M-Pesa, M-Coop Cash and Equity Bank’s Eazzy Loan.

The tracker survey further showed that 35 per cent of Kenyan phone owners are digital borrowers, therefore yielding an estimated market of 6.1 million unique digital borrowers in Kenya.

The most commonly-used digital lending product is the M-Shwari product, though competitors such as KCB M-Pesa, Equity Eazzy, Tala, M-Coop Cash and Branch are increasingly being used owing to the ease of borrowing on the platforms.

“Demonstrating the ease of accessing digital credit, 14 per cent of digital borrowers were repaying multiple digital loans at the time of the survey.

“Analysis of the demographic profile shows that digital credit users are more likely to be male, young, more educated, and to run their own business or be employed,” the CBK said.

As at March 2017, the volume of new mobile loans approved monthly by commercial banks had increased by 53 per cent, while the value of new mobile loans approved monthly increased by 81 per cent, according to the CBK report.

In March 2017, 8.6 million mobile loans were approved, representing a total value of Sh34.5 million.

But even as the uptake of digital loans expanded, the CBK warned that many consumers of such credit were digging themselves into deeper financial holes.

Statistics from the CBK indicate that the non-performing loan (NPL) ratio for digital loans offered by lenders is consistently higher than that for the entire bank loan portfolio.

“In 2016, the NPL ratio for bank digital loans averaged 26.98 per cent as compared to 8.53 per cent for all bank loans. In 2017, the difference was less pronounced, with an 11.4 per cent NPL ratio for digital loans as compared to a 9.69 NPL ratio on average for all bank loans” the regulator said in its latest survey report.

The FinAccess Digital Tracker Survey 2017 data show that 49 per cent of male and 45 per cent of female digital borrowers have delayed in repaying their digital loans, with poor business performance, loss of the source of income and poor planning cited as the main reasons for late repayment.

“In general, 25 per cent of digital borrowers reported that repayment periods were too short, while 19 per cent noted a lack of transparency in terms of fees or loan terms,” the CBK report said.

Digital borrowers are almost twice as likely to have tried mobile betting at least once in their life, the survey revealed, as compared to non-users of digital credit. This suggests that digital lending may tempt individuals to take digital loans to finance gambling or other risky behaviours, and in turn reduce the ability to repay loans. This can increase household indebtedness.

Unlock a world of exclusive content today!Unlock a world of exclusive content today!