The value of corporate bonds issued on the Nairobi Security Exchange (NSE) has dropped by Sh13.68 billion over the five years since 2014, triggering fears there could be total dry out by 2022 when the last of the current listed facilities mature.

Currently, there are 20 bonds issued by 12 companies with a total value of Sh57.6 billion compared to August 2014 when Kenya had 28 listings with a sum value of Sh71.28 billion.

Although the Capital Markets Authority (CMA) had in 2014 drawn up plans to boost corporate bond markets to 40 per cent of the Gross Domestic Product by 2023, the market risks having none in a few years.

Since April 2017 when East African Breweries Limited (EABL) issued a bond, no other Kenyan firm has sought a long-term debt from the capital markets.

In the next six months, a total of nine corporate bonds will mature in the country; six in 2020, four in 2021 and another two in 2022. Then there will not be a single corporate bond in Kenya, East Africa’s biggest economy and most liquid capital market.

Firms with maturing bonds are seeking private cash rather than go back to the corporate bond market where an issuance drought extends to 27 months.

Robert Kibaara, CEO of Housing Finance Group whose bond matures in October says the company does not intend to take another bond since the price is problematic, the costs are high and success is doubtful.

“We are almost closing Tier II capital which is easier and you just have to talk to one institution instead of a bond, with risk of non-payment, only government is issuing,” he said.

This sad state of affairs has been caused by the problem of interest rates and a tough environment that has led to a trend of defaulters who have sunk investors cash in black holes.

Foreign investors are no longer confident in giving money to Kenyan companies that they sold off their holdings to reduce exposure. Currently, local corporate bond investors hold 99.33 per cent of amounts outstanding as at the second quarter of the year, according to the Capital Markets Authority(CMA) Soundness report while foreigners had 0.67 per cent of total corporate bond holdings.

This goes on to show that companies know that if they make an attempt to raise cash at the market, their issues could flop despite the fact that there is excess liquidity chasing government bonds.

In the second quarter this year, the government sought to raise Sh140 billion but received subscriptions worth Sh242.07 billion.

“In the end, however, it accepted to issue bonds worth Sh157.82 billion, indicating a 65.20 per cent acceptance rate,” CMA said in the Soundness report.

It is only the government that has issued 83 bonds that continue to dominate the market, including two retail ones where ordinary Kenyans buy the securities via mobile phones dubbed M-Akiba. And herein lies the problem.

“During the quarter, Corporate Bond turnover amounted to Sh34.76 million, 0.02 per cent of total bond turnover valued at Sh190 billion, making Treasury bond turnover at 99.98 per cent,” CMA said

In 2016, Kenya’s legislature voted to cap interest rates charged by banks to four percentage points above the indicative Central Bank Rate released bimonthly.

Banks shut down the taps for the private business and between April 2016 to April 2019, private sector credit increased only 10 per cent from SAh2.260 trillion to Sh2.460 trillion, meanwhile money lent to the government went up 60 per cent from Sh690 billion to Sh1.1 trillion.

With the State gobbling up banks’ cash, the market has been mispriced, most of the active bonds are yielding higher than retail customers.

The NSE chief executive officer Geoffrey Odundo admitted that these defaults led to a decrease in investor demand for corporate bond issuances. He challenged the market to put up a guaranteed bond even as the NSE tried to talk Africa Development Bank and other big issuers to do a local currency bond to save the market.

Firms with maturing bonds are opting for private cash rather than go back to the market.

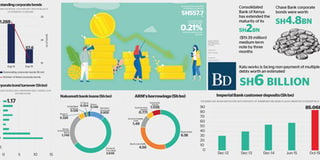

Insurer UAP Holdings redeemed its Sh2 billion bond using new loans while Consolidated Bank with a negative core capital of minus Sh29 million and operating at a Sh54 million loss as at March 2019 has turned to a government bailout to pay back a Sh1.7 billion bond issued in 2012 which is in default.

New entrants like fintech firms who have been active in the market often rely on raising capital privately, giving a cold shoulder to corporate bonds.

Since 2017, branch has raised Sh1.5 billion arranged by the Centum-owned advisory firm, Barium Capital with the latest funding coming in June.

Branch raised Sh200 million, closed in July 2017, Sh350 million in June 2018, Sh509.4 million in December 2018 and its fourth commercial in July 2019.

Investors, however, draw consolation from new debt avenues, including the Green bond being fashioned for the first time this year. The first issue being the Acorn Sh5 billion bond which has also come with enough security to ensure investors are reassured of the safety of their money.

Acorn’s bond will be guaranteed by an A rated GuarantCo backed by the governments of the United Kingdom, Australia, Sweden, Switzerland and the Netherlands.

Another layer of comfort will be a debt service account funded with three months interest and an assignment of rental income towards payment of the debt.

The investors will also hold a first ranking charge on land and a floating charge over all the assets of the issuer to safeguard their interests.

Imperial Bank

When fund managers, corporate and retail investors lined up to give Imperial Bank Sh2 billion in a five year bond they expected to reap the highest annual returns in the listed market. Imperial bank was offering fixed coupon rate of 15 per cent.

In October 2015, Imperial Bank of Kenya collapsed days before listing a Sh2 billion bond.

The closure of Imperial Bank left the markets authority and the Nairobi Securities Exchange with mud on their faces, having approved the Sh2 billion fundraising that almost traded on the day the bank was shut down.

Chase Bank

Chase Bank’s 13.1 per cent Sh4.8 billion bond was frozen in April 2016 when the lender went under. The bondholders are yet to secure their cash.

Athi River Cement

Cement- maker Athi River Mining defaulted on a privately-placed unsecured bond in June 2018 and was subsequently put under administration.

Nakumatt

Nakumatt was also buying such costly debt papers in private placement which allowed investors to lock in sums of money to the retailer. The retailer’s private placement hit mostly lenders who are owed Sh35 billion who will either have to book non-performing loans or restructure their facilities, an exercise that will take the next decade before they can recoup their money.

Nakumatt was also put under administration, which means the bonds and commercial papers they issued cannot be redeemed.

Real People

Real People wants to postpone repayment of its Sh1.3 billion bond to 2028. The South African SME lender has turned serial defaulter seeking to delay payment of its bond for a third time as it holds talks to settle the debt in nine years.

Last year when the bond matured in August, Real People said that it had met the investors of the Sh1.3 billion notes to renegotiate terms for the bond and they resolved to wait for payments till January.

In January, Real People again sought relief from its lenders for another eight months to August this year and it is now seeking yet another extension to February 2020.

Consolidated Bank

Consolidated Bank, whose fortunes are on the rickety ground, is supposed to pay back a Sh1.6 billion bond issued in 2012 that matured last month.

As at March 2019, the lender had a negative core capital of Sh29 million down from Sh176 million in March last year and was operating at a Sh54 million loss. Consolidated Bank pushed repayment of the Sh1.6 billion bond by three months.

TransCentury and East African Cables

In 2016, TransCentury was unable to pay back its Eurobond, forcing a restructuring through Kuramo Capital which helped the company restructure the bond.

TransCentury, which holds a 68.38 percent stake in East Africa Cables, also helped its subsidiary to restructure its Sh1.6 billion debt to 10 years, including a moratorium of two and a half years.

This resulted in reduction of debt by Sh1.65 billion representing 44 percent of total debt but the firm still remains insolvent by Sh542 million.

Unlock a world of exclusive content today!Unlock a world of exclusive content today!