Kenya’s monetary policy is back in the spotlight after a new report showed that the country’s foreign investment attraction ranking had stagnated comparative to its East Africa peers amid concern about rigidity in currency movement.

The Absa Africa Financial Markets Index (AFMI) 2019 showed that Kenya retained positioned three with a score of 65 out of 100 points, placing it below leader South Africa and second placed Mauritius, which added 13 points to hit 75 points.

And while Kenya stagnated, its neighbours Tanzania, Rwanda and Uganda closed their gaps by gaining 12, four and three points respectively to storm into top 10 spots. Tanzania climbed from position 15 to seven as Rwanda moved to 9th from previous year’s 11th.

A review of the ranking showed Kenya’s woes largely stem from low sensitivity of its currency to market fundamentals — potentially pointing to interventions on currency positions by the Central Bank.

And while Kenya improved its points in five of the six pillars used in ranking the attractiveness of markets, it lost 28 points in ‘access to foreign exchange’ pillar to close with 65 points. This saw it drop from last year’s first position in this pillar to fifth, beaten by South Africa, Egypt, Uganda and Rwanda.

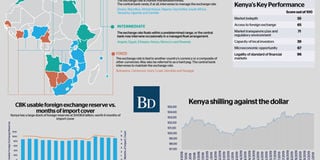

The AFMI 2019 report cited last year’s move by International Monetary Fund (IMF) to reclassify the Kenyan shilling from ‘floating’ to ‘other managed arrangement’ to reflect the currency’s limited movement due to periodic intervention by Central Bank of Kenya (CBK).

“Kenya drops in ranking (on forex pillar) after the IMF reclassified its exchange rate regime to ‘other managed arrangement’ from ‘floating’, a move the central bank contests,” said the report.

The report says the reclassification pulls down Kenya’s rank but its score is still among the highest in the pillar since other indicators remained healthy.

“It has a large stock of foreign reserves, worth four months of imports and 10 times its 2018 figure for net portfolio investment,” the report observed.

The controversial IMF sentiments were captured in its October 2018 Article IV economic health check where it stated that the shilling was overvalued by around 18 percent.

CBK governor Patrick Njoroge disputed the assessment arguing he only intervenes in foreign exchange markets to counter volatility, and that the IMF exaggerated the shilling’s overvaluation.

The shilling was one of the best performing African currencies last year and has been stable against the dollar, which climbed against most African currencies during the second half of the year.

The index evaluates financial market development in 20 countries, and highlights economies with the clearest growth prospects.

Scores are based on six pillars: market depth; access to foreign exchange; tax and regulatory environment and market transparency; capacity of local investors; macroeconomic opportunity; and enforceability of financial contracts, collateral positions and insolvency frameworks.

Kenya’s best pillar was ‘enforceability of financial contracts, collateral positions and insolvency frameworks’ where it improved from last year’s 83 to 96 points. This placed it second on the continent, beaten by Mauritius (98 points).

The pillar measures how well countries have adopted internationally accepted legal standards based on their recognition of master agreements, the enforcement of netting and collateral positions, and the adequacy of insolvency regimes.

The report says Kenya has a slightly stronger insolvency regime as measured by strong score in the World Bank’s ‘Doing Business 2019’ report.

“Financial market growth requires adequate legal frameworks that mitigate uncertainty for market participants, especially those entering new jurisdictions,” the Absa report notes.

Kenya is cited as among countries that have recognised global contractual standards such as that of International Swaps and Derivatives Association, which is the most widely used global framework for over-the counter trading.

In addition, the country also uses Global Master Repurchase Agreement (GMRA), which governs repurchase agreements and is essential during cross-border transactions as well as domestic repo markets.

Kenya’s use of Global Master Securities Lending Agreement (GMSLA), which provides a contractual framework for securities lending arrangements also helped it to score high.

Second highest score (71 points) came from market transparency pillar even though Kenya dropped five positions to rank at 11, the worst position among the six pillars. It was beaten by Uganda, Rwanda and Tanzania in the region.

The pillar assesses attractiveness of countries’ regulatory and tax environments for financial markets.

“Kenya’s tax code is generally supportive, according to one local tax professional. However, in an effort to raise revenue, the government has introduced prohibitive taxes, such as an increased levy on mobile cash transactions,” says the report.

On the pillar of macroeconomic opportunity, Kenya gained two points to score 67 but came down two positions to 5th, meaning other economies gained more points.

The report cites rising debt to gross domestic product (GDP) ratio, a position exacerbated by China’s Belt and Road initiative. Kenya, Mozambique, Nigeria, Ethiopia and Angola are among index countries that have received Chinese financing for infrastructure projects.

The country fared well on ‘market depth’ depth pillar which examines size, liquidity and diversity of products in capital markets, as well as efforts to merge exchanges and launch new markets.

It earned 11 additional points to close with 55 points and at position five, up from last year’s rank (eighth), showing that efforts by Capital Markets Authority and Nairobi Securities Exchange (NSE) are headed in the right direction.

The report lauds Kenya for joining the ranks of countries that scored over 50 points in this rank to chase South Africa which has sizeable lead owing to market capitalisation, that is triple the size of its economy.

“Kenya earns points following a sharp climb in the value of listed sovereign bonds and a 20 percent rise in bond turnover in the 12 months to June 2019,” notes the index report.

The value of bonds listed on the NSE doubled to $17.5 billion from $8.8 billion over the year, due to sovereign issues.

New products have been introduced on the NSE including the mobile traded bond, derivatives market and the gold exchange traded fund as well as the ibuka programme that is taking firms through a pre-listing programme.

However, new listings have been a challenge with interest rate cap laws being cited as having weakened companies’ financial bottom line, hindering expansion plans and negatively impacting their capital issuance.

Kenya also scored lowest points on the capacity of local investors pillar, gaining six more points to close at 39. It was ranked eighth, down one position.

This means that policymakers have much more work to do in crafting and implementing financial inclusion strategies to complement the build-up of pension assets.

While Kenya’s pension assets have been rising, fragmentation of those assets in many small pension fund schemes and motives to invest in securities other than government debt and real estate has limited pension funds’ contribution to capital market growth.

Unlock a world of exclusive content today!Unlock a world of exclusive content today!