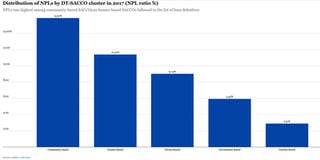

Community-based deposit-taking saccos are hardest hit by non-performing loans (NPLs), new data by the regulator showed, signaling the risks of loose membership.

They saw their NPL ration rise to 15.91 per cent in 2017 from the 9.84 per cent recorded the previous year, data in the Sacco Societies Regulatory Authority (Sasra) showed.

“This underscores the difficulty with which these saccos whose field of membership is usually quite loose are normally operating,” the regulator said.

An increase in demand for savings products has seen the emergence of many community saccos, most of which offer borderless membership unlike was the case before when saccos were modelled under umbrella associations, social organisations and companies, with membership restricted to staff and officials.

Farmer-based deposit- taking saccos recorded the second highest NPLs ratio at 11.42 per cent in 2017 despite declining marginally from the 13.6 per cent the previous year.

The NPLs among the government-based deposit-taking saccos rose to 5.95 per cent in 2017, from 4.28 per cent the previous year.

“The NPLs, however, remains lowest among the teachers’-based saccos at 2.91 per cent in 2017, which is a drop from a high of 3.54 per cent” Sasra said.

The regulator said that the increase in the NPLs in respect of the government-based saccos is directly attributed to the ripple effects of delayed remittances of loan repayment deductions by the national and county governments, as well as certain State institutions.

“The devolution of certain governmental functions, which were hitherto centralised, has lead a situation where some government-based saccos have had deal with several distinct payroll entities; as a means of making loan recoveries from their members,” Sasra stated.

“This decentralisation of payrolls has most of the times occasioned inordinate delays in the remittances, and implementation of the loan deduction requests, leading to default by members”.

Some governmental institutions particularly public universities, research institutions and parastatals, the regulator said, have equally contributed to the increased NPLs among this cluster of saccos with their sporadic and unreliable remittances of loan repayment deductions.

Saccos in private sector-based organisations have not been spared the jump in NPLs even as the effect of recent economic slowdown, partly due to a prolonged electioneering took toll.

“The tough macro-economic conditions that many private institutions and companies operated in during the year 2017 can be directly attributed to the increase in the NPLs for the private-sector-based saccos which increased from five per cent in 2016 to a high of nine per cent in 2017,” Sasra said.

Saccos in this category heavily rely on the private companies as the principal catchment area for their membership. They also rely on these companies to deduct and remit loan repayments from the employees’ salaries, which is the condition upon which they advance the loans to their members.

“Thus, whenever these companies lay off employees; or fail to deduct; or deduct but fail to remit the employees’ loan repayments, the ripple effect is translated to default on the loans in the books of the sacco,” the regulator stated.

Overall, deposit-taking saccos saw the NPLs ratio rise to 6.14 per cent in 2017 from 5.22 per cent—slightly higher than the recommended industry average of five per cent.

Unlock a world of exclusive content today!Unlock a world of exclusive content today!