Cash-rich NSE firms take hit from bank interest rates cap

An investor at the Nairobi Securities Exchange. PHOTO | FILE | NATION MEDIA GROUP

What you need to know:

The law has since forced most banks to reprice their deposit rates down to the statutory minimum, leaving it to a small bunch of distressed and risky lenders to offer higher rates.

Bank deposits have been popular because of their liquidity and the fact that they allowed high net worth investors to negotiate rates in the double digits, which nearly matched returns on short-term treasuries.

Cash held in bank has been safe for the most part, save for the trouble that came with the collapse of Dubai Bank, Imperial Bank and Chase Bank.

Commercial banks have significantly cut interest rates payable on cash deposits, leaving cash-rich companies and individuals with less returns from the billions of shillings kept with the lenders.

Official banking data shows that most banks are paying for the deposits at the statutory minimum rate of seven per cent, eating deep into depositors’ earnings.

Fund managers, who previously earned up to 20 per cent on their deposits during recurrent liquidity crunches, top the big losers’ list, which also includes cash-rich companies.

The Banking (Amendment) Act 2015, which took effect last September, sets the floor for deposit rates at 70 per cent of the Central Bank Rate, which currently stands at 10 per cent.

Reprice deposits

The law has since forced most banks to reprice their deposit rates down to the statutory minimum, leaving it to a small bunch of distressed and risky lenders to offer higher rates.

Carbacid Investments and asset manager Stanlib Kenya are among the firms that have reported a decline in their earnings from cash deposits, but cash-rich firms such as Safaricom, WPP Scangroup and insurers are expected to face a similar fate.

Carbacid says in its latest financial report that it expects “the Banking (Amendment) Act 2016, which came into effect in September 2016 to restrict our returns on deposits to around seven per cent.”

The Nairobi Securities Exchange-listed firm said it earned an average of 13 per cent on its short-term bank deposits last year – a rate that is expected to halve this year if it does not move the money to alternative investments.

Carbacid earned Sh127 million on its short-term deposits of Sh916.9 million, and is now looking at moving the cash to alternative investment channels, including T-bills, to escape the low-yield contracts.

“Alternative investment strategies are being considered by your board,” the company told its shareholders in the report.

Stanlib took a similar hit from the rate cuts as reported by its parent company, South Africa’s Liberty Holdings.

“The asset management business in Kenya (Stanlib) experienced operational issues coupled with financial market disruption and regulatory interventions that have impacted the business model,” Liberty said in a trading update.

It remains to be seen to what extent cash-rich firms and individuals are willing to venture into alternative short-term investments to earn higher returns with minimal risk.

Bank deposits have been popular because of their liquidity and the fact that they allowed high net worth investors to negotiate rates in the double digits, which nearly matched returns on short-term treasuries.

Cash held in bank has been safe for the most part, save for the trouble that came with the collapse of Dubai Bank, Imperial Bank and Chase Bank.

Chop deposit rates

Big banks are not expected to budge on their decision to chop deposit rates, which are essential for them to avoid thinning their margins further because the lending rate is also capped at 14 per cent.

The major lenders, especially the top five banks, are under little pressure to raise their deposit rates – having been boosted by the drop in risky lending and deposit flight from smaller banks.

Large depositors are also unlikely to move to small banks that do not have the depth to absorb the hundreds of billions of shillings they control.

The treasuries market, however, has the ability to absorb the cash and offer returns that are significantly higher than the statutory minimum deposit rate of seven per cent.

Coupons on the latest auctions of the 91, 182 and 364-day T-bills stood at 8.6, 10.4 and 10.9 per cent respectively, offering an opportunity for investors to structure their portfolios according to their returns and liquidity needs.

Largest depositor

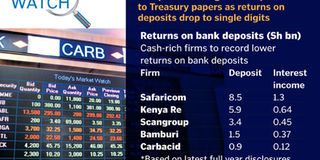

Safaricom is one of the largest bank depositors in the country having kept Sh8.5 billion with lenders last year, raking in some Sh1.3 billion in interest income.

Kenya Re in 2015 deposited Sh5.9 billion with banks, earning Sh647.9 million on the cash while marketing and communications firm WPP Scangroup deposited Sh3.4 billion with the financial institutions to earn Sh451.6 million in interest income. Bamburi Cement held Sh1.5 billion in banks in 2015, which earned it Sh374 million.

The capping of interest rates now appears to have had a huge impact beyond the lenders’ fortunes, creating a growing list of winners and losers depending on which side of the creditor/debtor relationship one sits with the banks.

Companies that borrowed millions of shillings at high interest rates prior to the enactment of the law booked major savings in September when their debts were repriced down to 14.5 per cent and later to the current 14 per cent.

The list includes ARM Cement, East African Cables, property developer Home Afrika, Uchumi Supermarkets, fast-moving consumer goods manufacturer Flame Tree and fashion retailers Deacons and Nairobi Business Ventures.

New borrowing by those with weak credit histories has, however, become more difficult as banks pull back from risky lending in an environment where they cannot add a premium rate to address the risk of default.

Personal lending is one of the hardest hit, with KCB Group and Equity Group limiting the repayment period on their popular mobile-based loans to one month from the previous six to 12 months.