Equity Bank rallies to catch up with EABL in stock market race

Members of the National Assembly’s Energy and Communications committee address a news conference on the dispute between Safaricom and Equity Bank over the latter’s thin SIM card at Parliament buildings in Nairobi September 24, 2014. PHOTO | EVANS HABIL |

What you need to know:

Equity had overtaken EABL in valuation in the first two trading days this week.

Analysts predict that EABL could cede the position in the longer term as the bank continues to draw huge investor interest.

The top spot is held by telecommunications giant Safaricom, which has a market capitalisation of Sh502.8 billion, more than the next two combined.

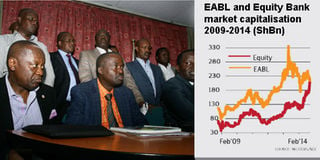

Equity Bank is neck-and-neck with East African Breweries Limited (EABL) in a capital markets race for Kenya’s second-most valuable listed company, signalling a fresh shift in dominance from manufacturing to the services sector.

The lender’s stock has rallied 77 per cent so far this year to Sh54.50 a share and was valued at Sh201.8 billion Tuesday, to EABL’s Sh211.9 billion at Sh268 per share, which is down 7.6 per cent since January.

Equity had overtaken EABL in valuation in the first two trading days this week — reaching its highest value of Sh218 billion on Tuesday — but fell behind Wednesday as its share price took a hit on concerns over its mobile virtual network operator (MVNO) licence.

This allowed the brewer to surge back ahead of Equity, but analysts predict that it could cede the position in the longer term as the bank continues to draw huge investor interest.

The top spot is held by telecommunications giant Safaricom, which has a market capitalisation of Sh502.8 billion, more than the next two combined.

Last week, Equity became the first NSE-listed bank and third company of any kind valued by investors at more than Sh200 billion. This is the first time that the bourse has three companies above this level. Total market capitalisation is now at Sh2.29 trillion.

Kenya Commercial Bank (KCB) is also in the middle of a price rally of its own. With a total value of Sh171.6 billion, the bank could also break above the Sh200 billion mark if it sustains its current momentum.

Mavuno Capital chief executive Robert Bunyi said the new market dynamics reflect the increasing prominence of the sectors the companies are involved in, citing the financial services industry as a strong engine.

“As we move to middle income status as a country, the financial sector will tend to grow faster alongside retail and services, as people gain purchasing power,” said Mr Bunyi.

“Growth in manufacturing is slower (because) we are an open and relatively small economy and we tend to import rather than produce locally and demand can almost be met entirely by imports.”

Both Safaricom and Equity Bank listed less than 10 years ago and their rise above the much older EABL in valuation is indicative of the shift in the economy where financial services and telecommunications have caught up with the more established manufacturing segment in driving growth. EABL first listed on the then Nairobi Stock Exchange in 1954.

From May 2013 to date, EABL has seen its value drop by Sh122.6 billion, with Safaricom, Equity and KCB seeing their market caps go up by Sh216.8 billion, Sh72.2 billion and Sh47 billion respectively. The NSE’s four biggest firms are now worth nearly half of its total market cap.

Standard Investment Bank (SIB) director Job Kihumba said the trend whereby more financial services firms are rising up the ladder of NSE companies was set to continue, given the dynamics of the wider economy at the moment.

“Increased activity in the other sectors of the economy means that you see a similar increase in the financial services as well, given that this sector is the oil that keeps the economy going. As a country, we are mobilising a lot of resources to drive the economy, and through this process... we see a huge upside for the financial services sector going forward,” said Mr Kihumba.

He said that the increased activity is being seen in the infrastructure, transport and telecommunications sectors, adding that part of the ripple effect of such developments is the rally in Equity’s stock, which is being driven by the recent award of an MVNO licence to Finserve, the bank’s financial services subsidiary.

The banking sector has also drawn some of its growth from increasing profitability, with a number of institutions now pulling in more net earnings than EABL, which for long was the most profitable firm in the country.

In the 2009 financial year, EABL earned Sh8.2 billion in net profit, twice as much as the Sh4.1 billion earned by KCB and Sh4.2 billion by Equity.

In the full year ended June this year, EABL’s net earnings grew by five per cent to Sh6.85 billion following improved performance by most of its products.

In comparison, KCB and Equity’s net profit for the year ended December 2013 stood at Sh14.3 billion and Sh13.3 billion respectively.

In their half year to June 2014 results, KCB reported a net profit of Sh8.17 billion while Equity’s was Sh7.66 billion.

EABL’s financial performance has been largely affected by unfavourable changes in the tax regime especially on the lower-end-of-the-market Keg beer.

Senator Keg had a tax exempt status since 2004 when it was introduced in the market as an alternative to illicit alcoholic but the Treasury imposed a tax last year to raise revenues and enhance tax equity.

“EABL has been affected by the tax regime raising the cost of keg and driving a vast majority of consumers to low-cost unregulated and untaxed alcohol. To help EABL — and the manufacturing sector as a whole — we need lower levels of taxation and can look at reducing the cost of logistics while coming up with more favourable trade agreements with the export markets,” said Mr Bunyi.

Comparatively, across the various market segments at the NSE, manufacturing lags behind the leading performers in insurance, banking and investments in the year to date. The insurance sector has returned a growth of 102 per cent, banking 29.3 per cent and investments 77.6 per cent.

For its part, the manufacturing segment returns this year are up 1.8 per cent, only outperforming commercial and services (whose returns have declined by 9.7 per cent) and construction (which is down 18 per cent).