Key to note is that these micro-finance institutions target customers in the lower segment of the pyramid meaning the amounts given are significantly lower compared to other mortgage firms.

Owning a home has been an elusive dream for many Kenyans due to the high costs involved. But this is set to change because of the entry of micro finance institutions into the mortgage arena.

These new entrants have come with better rates and flexible payment arrangements compared to what is being offered by the big banks or established mortgage institutions.

With these new entrants, one does not have to go through the arduous procedures set by mainstream lenders before you get your loan. In fact, low income levels or lack of credit history by a borrowers are no longer a hindrance to owning a home.

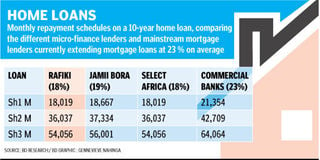

Chase Bank’s subsidiary, Rafiki, recently joined other microfinance institutions; Jamii Bora and Select Africa to sell home loans to workers in the informal sector and salaried low income earners.

Rafiki’s entry comes a year after Jamii Bora Bank unveiled its home loan product targeting buyers into housing estates developed by its subsidiary, Makao.

With Rafiki’s offer, for instance, one can own a home built using new technologies at a cost of between Sh1 million to Sh3 million, payable over a 10-year period.

This means buyers of the cheapest house would pay a monthly mortgage of about Sh19,000 for 10 years.

The loans will be priced at 18 per cent on a variable interest rate schedule. This is unlike the average 23 per cent interest charged by banks.

Rafiki plans to finance 100 per cent of the construction costs for individuals with land, and an additional 70 per cent of the cost of land for people who do not already have land.

According to George Mbira, a real estate development expert and General Manager at Rafiki Data Taking microfinance , the appraisal of customers by microfinance institutions is different from that of banks.

“For micro-finance institutions, household income forms the integral part of the loan appraisal while other mortgage firms use conventional tools such us audited accounts, pay slips and bank statements to account for turnovers,” explains Mbira.

Incremental mortgage

Mbira says Rafiki DTM offers incremental mortgage plans where a customer build their home in phases which may start with the acquisition of land and gradual construction as cash flow allows.

“We also finance stand alone houses up to Sh3 million with an interest range between 18 and 27 per cent depending on which plan the customer undertakes,” he says.

Keen to meet the ballooning demand for home ownership, Select Africa, a subsidiary of African Alliance, also entered the Kenyan housing sector early last year.

Its model allows households to develop their home incrementally over several years, with the micro-financier providing the funding as well as the building technology.

Key to note is that these micro-finance institutions target customers in the lower segment of the pyramid meaning the amounts given are significantly lower compared to other mortgage firms.

Mbira says taking a mortgage is the best decision one can make towards owning a home. “One should try and commit to a mortgage early in life. One should also try and understand all the terms and conditions of the mortgage including the implications on personal cash flows in the short and long-term,” he advises.

However, he cautions consumers to plan their financial commitments well before taking a mortgage since lack of planning can lead to a financial crisis. “Consumers tend to over commit themselves in huge mortgages without factoring in the eventuality of increase in interest rate and rise in inflation. They then find themselves in a situation where their disposable income is too low to sustain monthly repayments,” he argues.

In the quest for cheaper homes, consumers often end up taking mortgages in areas too far from basic amenities such as schools and their places of work. Always make sure the location you choose is good in case you need to sell your property in the future.

“Some consumers do not carry out due diligence on government policy regarding areas where the home they are buying is located which has seen some houses demolished,” Mbira further warns.

Cathy Warega, Head of Sales and Marketing at Jamii Bora Makao, which is currently managed by Urbanis Africa, says consumers should compare mortgage costs including interest rates, fees and other closing charges.

“Apart from interest rates, mortgage-related expenses can amount to about 9 per cent of the cost of the property. This requires careful consideration because failure to plan for this can lead to financial distress,” she advises.

She says although Jamii Bora Makao are not financiers and do not offer any mortgages, it has partnered with different mortgage firms to including JamiiBora Bank, Housing Finance and Savings and Loan to offer both micro-finance mortgages and traditional mortgages at different rates.

The Central Bank of Kenya’s Bank Supervision Annual Report 2011 shows that there were 16,135 mortgage loans as at the end of last year, which developers have said is a tenth of what an economy Kenya’s size should have.

Most of the respondents in the CBK survey covering the residential segment cited low income levels, the lack of credit history on borrowers and the lack of housing as the main challenges that slowed the uptake of the mortgage business.

Nearly 23 per cent of the respondents said the cost of homes was too high compared to the average income levels.

PAYE Tax Calculator

Note: The results are not exact but very close to the actual.