Time flies with great content! Renew in to keep enjoying all our premium content.

Prime

Bank profits surge to record Sh108bn on expensive loans

Customers at an Equity Bank’s banking hall in Nairobi. Profitability in the banking sector jumped to Sh108 billion last year on the back of high lending interest rates. Photo/FILE

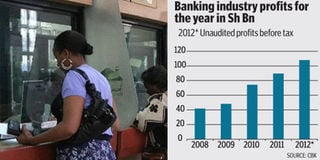

Profitability in the banking sector jumped to Sh108 billion last year on the back of high lending interest rates bringing back concerns that the financial sector could be growing at the expense of productive activities.

Commercial banks raised average lending rates from 14 per cent to 26 per cent last year in response to the Central Bank raising the its distress rate threefold to 18 per cent in a bid to protect the shilling.

This saw the interest margin — the difference between lending and deposit rate — grow to double digits, assuring banks of a windfall.

The Kenya Bankers Association (KBA) said that banks tend to enjoy higher revenues from wider interest spreads during volatile moments but this was not the only cause of profit growth.

“When interest income becomes a challenge you concentrate your efforts to other income streams like service delivery areas which earn fees,” said KBA chief executive officer Habil Olaka. The sector profit for the year represents a 20.3 per cent increase over the Sh89.5 billion made in 2011.

However, data from the Central Bank shows that as at November last year interest income contributed 62 per cent of the industry total income compared to 55 per cent in a similar period in 2011.

The net interest margin rose to 13.05 per cent from 10.25 per cent, according to the data.

The fact that commercial banks are charging borrowers 20 per cent on average for loans while paying savers less than 5 per cent for term deposits despite the inflation rate falling from 19 per cent to less than four per cent has also raised eye brows.

“Unless there is some sort of control they will always make abnormal profits at the expense of the economy. We thought they would self-regulate but this seems not to be the case,” said Joe Donde, a a member of consultative committee on consumer protection in the financial market.

In the last two years, Parliament has sought to control interest rates against the wishes of the Treasury. Although the Treasury carried the day on both occasions the standoff led to delays in the passing of the Finance Bill.

The Consumer Federation of Kenya (Cofek) said it would take up the matter soon, citing the Consumer Protection Act which President Mwai Kibaki assented to last year.

“We are waiting for the law to become operationalised; they should be prepared for legal feuds. All indicators show that they shouldn’t be charging what they are currently charging,” Cofek CEO Stephen Mutoro said.

Mr Mutoro said that the reliance of banks on interest income had seen them squeeze households and weigh down other productive segments with heavy financing costs.

In an e-mail response to inquiries by Business Daily the Central Bank said the cumulative unaudited banking sector profits for the year ended 2012 was Sh107.68 billion, while total loans disbursed were Sh1.36 trillion compared to Sh1.19 trillion in 2011.

In 2012 the loan book grew by 14.3 per cent compared to by 30.2 per cent in 2011 indicating a slow uptake of credit owing to the higher cost of money.

However, the volume of loans not being serviced grew to Sh61.6 billion compared to Sh53 billion, underlining the pressure on households to repay debts in the face of the rising cost of living.

Customer deposits stood at Sh1.76 trillion up from Sh1.49 trillion, attributable to attractive deposit rates and agency banking which took banking services closer to the unbanked.

“Even if the loans did not grow at the same rate as the previous year they were being charged a higher rate leading to the higher income,” said Francis Mwangi, head of research at Standard Investment Bank.

Mr Mwangi also noted that when interest rates were raised most borrowers had opted to extend the period of repayment instead of increase their monthly repayments. The extension resulted in interest payment contributing a higher portion of the monthly instalment than the repayment of principal amount leaving the banks better off.

A survey by investment bank Renaissance Capital shows that Equity Bank’s net interest margin as at September was 12.4 per cent compared to 11 per cent in 2011 while Co-operative Bank enjoyed a spread of 10.2 per cent compared to 8.5 per cent a year earlier.

With interest rates coming down last year banks are expected to have recovered from the revaluation losses arising from their stock of government securities. In 2011 banks reported revaluation losses from portfolio of Treasury bills and bonds which have an inverse relation with interest rates.

Mr Olaka also pointed out that it would be inappropriate to look at the absolute figure reported by the industry without looking at the capital injected by shareholders.

“Shareholders have put in more money over the last year and had to be assured of returns so the banks are also under pressure from investors,” he said.

Last year a number of banks raised additional capital through various ventures which included rights issue by Standard Chartered, NIC Bank, CfC Stanbic, DTB, Jamii Bora while Equatorial Commercial Bank and Chase Bank invited strategic partners. Other banks that raised additional capital were Fidelity Bank, Dubai Bank and Oriental Bank.

Tuesday NIC Bank, KCB, Standard Chartered, Equity and Housing Finance trading counters, which constitute half of those listed under the banking segment, touched one-year highs underlining the market appetite for bank stocks.

Unlock a world of exclusive content today!Unlock a world of exclusive content today!