Time flies with great content! Renew in to keep enjoying all our premium content.

Prime

Parliament’s team rejects plan to tax basic goods

Chris Okemo, chairman of the Parliamentary Select Committee on Finance. Photo/FILE

Parliament is inching closer to removing tax on basic goods in amendments to the Value Added Tax Bill, setting the Treasury on a collision course with the International Monetary Fund (IMF).

Among the goods targeted are some foodstuffs, fertilisers, seeds and sanitary towels, which the new Bill had proposed to tax as part of recovering an extra Sh40 billion lost annually through exemptions and zero-rating.

The Parliamentary Committee on Finance accepted the bulk of proposals put forward by the Institute of Certified Public Accountants of Kenya (ICPAK) and audit firms, saying it would put the changes to the House for voting.

“We are in agreement with most of the proposals. We have also received similar proposals from other stakeholders and having discussed the suggestions for improvement of the Bill as a committee, it seems to us most of them have merit,” said committee chairman Chris Okemo.

The committee has met with, among other groups, the Kenya Association of Manufacturers, PricewaterhouseCoopers and the Kenya Dairy Board.

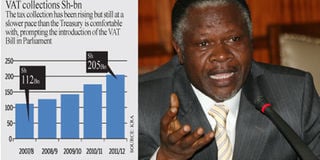

The tax reforms are at the centre of a financing agreement with the IMF and the MPs action could put the arrangement in doubt.

MPs are expected to stamp the changes given that imposing VAT would increase the prices of basic goods and adversely affect the majority of Kenyans just months to the General Election.

The committee also agreed to reduce the powers of the Treasury and the Kenya Revenue Authority (KRA), further cutting their effectiveness in taxing the country.

ICPAK had argued that the Bill gives the secretary of Finance (the position of Finance minister after the General Election) too much discretion in relation to making changes on the rate of VAT, which the MPs were convinced could be abused.

The Bill gives the Cabinet secretary discretion to increase or lower the standard VAT rate without reference to Parliament or any other authority.

ICPAK proposed that the Bill accommodate a definition of basic goods as “essential goods that support life”.

“We will probably have up to 20 basic goods which will be zero-rated. This means we will have drastically reduced the number of zero-rated goods from over 480 in the current law,” said ICPAK chairman Patrick Mtange.

According to him, the Cabinet Secretary for Finance should prescribe the commodities to be considered basic because of the diverse nature of the country.

The chair of ICPAK’s public finance committee, Erastus Omolo, told the MPs that basic goods were not taxed in the majority of countries with which Kenya benchmarks its tax system.

Mr Omolo said ICPAK had looked at the situation in Botswana, South Africa, Uganda, Tanzania and even the UK.

“If we impose VAT we are going to encourage a parallel market for goods from neighbouring countries. The taxman will lose revenue, jobs will be lost and other benefits will go if we tax basic items,” said Mr Omolo.

In further assault on the Bill, Robert Waruiru, a tax services manager with audit firm KPMG, said a requirement in the Bill that one pays 30 per cent of assessed tax in advance during disputes was tantamount to condemning an innocent person before he is heard and had the potential of being abused by overzealous KRA officers. MPs agreed to remove the clause.

“It is contrary to the provisions in the Constitution on what is a fair tax administrative action,” said Mr Okemo.

Sammy Mwaita, the MP for Baringo Central and a member of the Finance committee, said overzealous tax officials out to meet performance targets may be tempted to harass the taxpayers by making unfair estimates or assessments if the 30 per cent clause was not removed.

Mr Okemo said the committee agreed that refunds be paid within six months as is the case in Ethiopia, rather than within the current 12 months.

“We agree with the committee that after six months, then tax of two per cent per month should then accrue on a cumulative basis on what has not been refunded,” said Francis Kamau, the associate director of tax services at audit firm Ernst & Young.

Initially, ICPAK had proposed three months before the penalty can become applicable down from the current 12, but the parliamentary committee members counter-proposed a six-month period.

The MPs also passed a proposal that will allow companies carrying out long-term projects which originally benefited from tax incentives not to be taxed when the VAT law takes effect.

“I have talked with the KRA and they believe the tax incentives given to investors who came in to do long-term projects should remain in force,” said Mr Okemo.

“The projects are only being done because of the incentives that were given to them originally and so we should not then impose VAT.”

Mr Okemo, who was a finance minister in the Moi administration, said the VAT law had to effectively deal with the refunds problem because they had now accumulated to Sh26 billion.

“Government hasn’t provided for these refunds. We need to make a one-off provision for these refunds. The problem with zero-rating is that you end up with all these refunds accumulating,” said Mr Okemo.

Exemption from VAT means that there are no refunds claimed as is the case with zero-rated goods, where a company can claim a refund on input VAT paid.

Taxing of the church

The taxing of the church and other religious organisations was seen as problematic because there was no definition of what would be considered their “public” engagements – which are not normally taxed.

ICPAK also proposed a separation of the roles of a police officer and a KRA officer out to assess tax unless the taxpayer is uncooperative but the committee was non-committal on the matter. The VAT Bill proposes the tax officer to also have powers of arrest.

“We see the need for revenue police in circumstances where the taxpayer is uncooperative with the revenue officers,” said Mr Mtange.