Time flies with great content! Renew in to keep enjoying all our premium content.

Prime

Visa plans Kenya office in drive for E Africa market

Debit cards — which allow consumers to pay for goods and services from their bank balances. FILE PHOTO | NMG

Global payment systems provider Visa International has announced plans to open an office in Kenya in a move that will give the firm a stronger foothold in the east African market while enhancing Nairobi’s stature as a regional financial hub.

The company, which develops payments technology infrastructure that connects consumers to businesses such as banks through the use of digital currency instead of traditional cash and cheques, joins a growing list of multinationals eyeing emerging and frontier African markets to grow their revenues.

“We are looking at Kenya but need to go through the whole company registration process so it’s still in the early days,” said Visa International’s country manager for east Africa Victor Ndlovu.

Mr Ndlovu declined to discuss the firm’s strategy for the region, but said a formal announcement of the move will be made next month.

Visa already has a presence in the region through its partnership with local banks, Safaricom’s M-Pesa service and PesaPoint, an ATM services company.

Sub-Saharan Africa is projected to grow faster over the next few years than developed markets which have been the traditional favourites for multinationals.

Prospects of more individuals in east Africa having a higher purchasing power is making the region attractive to the international firms.

Analysts said that setting up an office or an operation in the country will provide the company the advantages of having a physical presence in the region, giving its clients - consisting of banks and other payment service providers an opportunity to deal more closely with it while marketing its products.

Automated teller machine (ATM) providers such as Paynet which operate the PesaPoint ATMs are also linked up to the company’s network.

The multinational has partnerships with an estimated 16 banks in Kenya who issue debit and credit cards with the Visa brand enabling the cards to be used internationally through the company’s network.

Paynet’s general manager Romana Rajput said that the move would provide increased opportunities for the company and also for other banks to partner with the multinational.

“They do have a market share and they want to be well represented by bringing their products more into the region,” she said.

Visa’s Africa operations are handled from Johannesburg, South Africa.

“It will help in terms of training, understanding them better and it becomes easier if you are going to apply for a card,” she added. A manager at I&M Bank which is signed on to Visa’s payments infrastructure said that the move by the firm to set up an office in the region would provide “a more focused service.”

“They may be looking to tap into the market in the surrounding region,” he added.

The multinational is planning its entry in the country at a time when its rival, MasterCard, has been getting into similar partnerships with local banks and businesses.

Last month telecommunication firms Safaricom and Airtel launched partnerships with two different local banks that will give the companies’ clients access to Visa and MasterCard international services respectively.

Safaricom and I&M Bank introduced a service that allows M-Pesa customers to transfer money from their accounts to a Visa branded Safari Card.

Its rival Airtel launched a partnership with Standard Chartered Bank and MasterCard allowing for payment services through their mobile phones using the company’s Shopping Card.

“There are number of opportunities for the company in the region. The use of debit and credit cards is not yet that widespread.

“In Kenya use of cash is more prevalent and there is this push for movement towards use of less cash,” said Eric Musau an analyst with African Alliance Investment Bank.

Plastic money

The move to set up shop in the country will also help Visa take advantage of the growing use of plastic money in a region that predominantly uses cash.

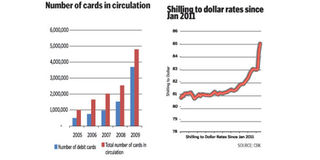

According to the Central Bank of Kenya (CBK), use of plastic money has been on the increase over the past 10 years in tandem with an increased number of ATMs due to “commercial banks’ business expansion strategies and the need to counter increased competition in the payment card industry.”

The number of ATMs in circulation as at the end of last year stood at 2,052 compared to 1,827 as at the end of December 2009 and 1,510 as at the end of December 2008.

CBK’s last annual report shows that for the period ended December 2009 the total number of cards in use rose by 88.6 percent to 4.8 million cards in December 2009 from 2.5 million cards in 2008.

Debit cards more than doubled to 3.7 million cards from 1.5 million cards in use in December 2008.