Time flies with great content! Renew in to keep enjoying all our premium content.

Prime

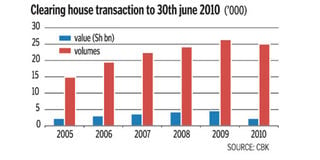

Automation to cut cheque clearance time by half

Equity Banking Hall. A new system called cheque truncation will reduce to two from the four days taken to process cheques. Photo/FILE

The number of days taken to process cheques is set to halve from May, when bankers are expected to roll out an automated system of clearing payments.

The new system called “cheque truncation” will reduce to two from four days taken to process cheques issued in major towns, and to four days from 10 the number of days for clearing upcountry cheques, Kenya Bankers Association (KBA) chief executive Habil Olaka said in an interview.

Mr Olaka, however, said reduction of transaction days under the new clearing system, which will also see all banks adopt cheques with common security features, will take time as drawers of cheques change from the culture of writing post-dated cheques.

“Customers usually take advantage of the long clearing period to issue cheques even when they do not have funds in anticipation of depositing in the course of the clearing process,” said Mr Olaka.

With the physical transportation of cheques no longer necessary, classification of branches into local, upcountry, and remote — where the cheques from remote branches take up to 10 days to clear will end.

Implementation of the cheque truncation process will also save banks costs of hiring courier companies, but Mr Olaka said it was still too early to quantify the amount of savings that would be passed on to customers by way of reduced transaction costs and interest charges.

The physical appearance of cheques will change beginning next month, said Mr Olaka.

The new system is part of reforms in the national payments system which also saw the banking sector regulator limit the value of cheques payable in Kenya capped at below Sh1 million last year.

All banks will be expected to inform their customers to return their current cheque books, which will be replaced with new ones during the pilot testing of the system between February and April, before the system goes live in May.

“The imaging equipment works on the basis of character recognition to capture details from the cheque. The details must be at a predetermined position fed into the computer and this will not be achieved if the cheques are not uniform,” said Mr Olaka.

All the new cheque leafs will have a standard size of 7 by 4 inches. Banks currently issue cheques of different sizes to different groups of customers.

Retail clients are commonly issued with small pocket size cheques, while corporates have larger ones.

“The size will be bigger and may create inconveniences for retail customers, but they should consider the benefits that will accrue from this process,” said the bankers’ lobby CEO.

Ongoing reforms

The ongoing reforms are expected to reduce fraud cases.

KBA has created standard security features that will be embedded on special paper which will be used to print the cheques, with the only distinction being identification logos of particular banks.

Accredited printers will be given printing tenders to limit forgery.

Currently, there are five security printers; De La Rue, Punchline, System Media Technologies, Kalzmart and Taws.

The quality of paper used dependents on particular banks, which also use their own resources to put in place security features on the cheques.

While banks with sufficient resources are able to put elaborate features on their cheques, others are greatly exposed to fraud.

Value capping

Last year, industry players introduced value capping which was meant to reduce fraud conducted by cheque substitution and diversion.

The value capping and electronic transfers, according to Mr Olaka, have also had their challenges.

“You cannot totally eliminate fraud as the face of fraud activities keeps on changing, but by making it expensive we will hope to manage it,” said Mr Olaka.

Physical cheques will not be moved to the paying banks, hence tellers in collecting banks will have the responsibility of confirming the genuineness of the cheques.

Banks will have room to put additional security features, their logos and those of their customers on allocated slots on the cheques.

“If banks wish to put in additional features they may, but other banks will rely on the standard security features to clear cheques,” said Mr Olaka.