Time flies with great content! Renew in to keep enjoying all our premium content.

Prime

KPC’s exposure in Triton scam drops to Sh6bn

Forensic auditors cut back to 96,000 mt the amount of petroleum products irregularly released to the collapsed firm. Photo/JACOB OWITI

The Kenya Pipeline Company’s exposure in the Triton oil scandal dropped to Sh5.7 billion after independent investigators hired to unmask the people behind it significantly reduced the amount of products that were irregularly released to the oil marketer before its collapse in December 2008.

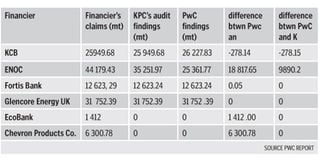

Triton’s financiers had initially claimed that they lost 122,200 metric tonnes of oil products in the deal worth Sh7.6 billion based on the then price of Sh60 per litre of petrol, but PricewaterhouseCoopers (PwC) — the audit firm that the government hired to unearth the scam — revised the figure to 96,000 metric tonnes worth Sh5.6 billion.

The new figures, contained in the forensic audit report that PwC presented to the government in April last year, significantly reduces the amount of claim each financier could make against Kenya Pipeline Company (KPC) with possible severe consequences on their books of accounts.

“We have concluded that the overall product liability was 95,900 tonnes,” the investigators say in the report.

That amount is significantly below the 122,200 metric tonnes claim initially lodged against KPC and upon which the total losses incurred was priced at Sh7.6 billion.

PwC investigators say they confirmed Fortis Bank of France’s claim to be 12.6 tonnes of petroleum products and Glencore Energy UK Limited’s 31.752 tonnes.

“Our best estimate of product liability to KCB is 26.3 tonnes, which is slightly higher than the 25.9 tonnes that the bank had initially claimed,” the report says meaning that KCB may have lost more than the Sh2 billion claim it has lodged in court against KPC.

It says KPC’s product liability to ENOC (Emirates National Oil Corporation) was almost half the 44.2 tonnes claim that the firm had initially lodged and dismisses EcoBank’s 1.4 tonnes product claim against KPC as lacking merit as the financier had authorized release of the product to Triton.

“We do not think that EcoBank’s claim has any merit because there is a release for the oil products that were the subject of the undertaking supplied to KPC. Any claim that EcoBank may have would therefore lie with Triton.”

The products were allegedly lost after KPC acted in breach of the Collateral Financing Agreement (CFA) that is the backbone of the petroleum supply chain and irregularly released products in its custody to Triton.

The agreement requires KPC to issue acknowledgement letters to the financiers confirming that they are holding stocks that they could only release to the marketer upon receipt of an authorisation from the financier.

KPC is, however, accused of having failed in its fiduciary responsibilities by not implementing the Collateral Financing Agreement leading to the loss of products.

PwC says senior KPC employees in the Operations and Finance departments – then headed by Mr Peter Mecha and Caleb Manyaga respectively – played a key role in the fraudulent release of petroleum products to Triton putting the burden of losses incurred on the shoulders of the state corporation.

“The liability of KPC to the financiers in respect of the irregular releases does not derive from the CFA contractual agreements – because the financiers were not parties to it – but from the breach of trust by the schedulers,” the investigators say.

The report – seen by the Business Daily – cites operational lapses at Kenya Pipeline as the major cause of Triton’s ability to draw products that did not belong to it causing distortions that nearly brought down the entire petroleum supply chain.

PwC investigators say KPC played a major role in the scam after its officials admitted to irregular release of an estimated 96,000 tonnes of various fuel products in its custody without the consent of lenders.

“Products for which acknowledgement letters had been sent but for which authorisation by the financiers to release had not been given were released on instructions of Triton contrary to the laid down procedure,” PwC says.

The report faults KPC for allowing outstanding irregular releases to more than treble in a span of two years from 40,000 cubic metres in January 2007 to 130,000 cubic metres in December 2008 – when Triton was placed under receivership.

The forensic audit report names Energy permanent secretary Patrick Nyoike, runaway billionaire businessman Yagnesh Devani and senior Kenya Pipeline Company managers as the main players in the chain of events that led to the sudden collapse of Triton and the near paralysis of Kenya’s petroleum supply system 18 months ago.

The report traces the origin of operational lapses at KPC to a phone call that the then operations manager Peter Mecha claims to have received from Mr Nyoike instructing him to release 1,000 cubic metres of diesel daily to the marketers to keep the power generators running.

Total and Triton were then the suppliers of diesel used by independent power producers to generate emergency power that the government required to meet the country’s energy needs.

Mr Devani is said to have lurched onto the PS’ instructions to exert undue pressure on KPC officials to irregularly release oil products to his company in breach of the agreement that required such action to be backed by written instructions from financiers.

The PS has denied any involvement in the matter saying the ministry had no role in the CFA arrangement.

“The first time I saw the CFA agreement was in December 2008 in the wake of the Triton crisis,” Mr Nyoike said on phone.

The report also gives insight into the business and financial difficulties that Triton faced before its sudden collapse in December 2008.

It links the oil marketer’s financial troubles to the volatile price movements that exposed it to large speculative risks in the market.

“Whilst facing these difficulties, Triton, with KPC’s support continued to draw irregular releases from the national pool leading to a near doubling of such releases from 70,000 cubic metres in July 2008 to about 130, 000 cubic metres in December 2008,” the report says.

PwC strongly recommends that the lenders take legal action against KPC for breach of the trust in the relationship created by the CFA.

The financiers have filed a series of litigations against KPC and Triton.

“The legal basis for claims by financiers would be for the torts of conversion and breach of trust. If these torts were proven, then the court could possibly award damages to compensate the financiers for losses incurred as a result of the tort,” it says.

The report blames Triton’s financiers, Emirates National Oil Corporation, KCB, Fortis of France and Glencore of UK, for not offering the investigators information on actual losses they incurred from illegal release of warehoused products.

“The oil marketers were not cooperative but with the assistance of KACC we were able to access critical information. KACC, however, imposed limitations on use of the information fearing that if reported at this stage it may jeopardize corruption watchdog’s own investigations,” the report says.

KCB, which has valued its loss at Sh2 billion, and filed a suit in court seeking to recover the money, did not provide the investigators with the documentation to support its claim against KPC.

“The bank did not allow us to speak to any of its staff, including those who had been suspended, on grounds of client confidentiality. The receivers of Triton appointed by KCB were not cooperative either possibly on instructions from the bank,” the investigators said. “An understanding of what happened at Triton is critical to meeting the objectives of this assignment,” the report concludes.

The forensic audit report was compiled more than 13 months ago but its contents have remained under lock and key at the Energy ministry and the Kenya Anti Corruption Commission (KACC), whose parallel investigations into the scam have not been concluded.

It names Benedict Mutua, Phanuel Okwengu and Thaddeus Akama, Philip Kimelu, Joseph Kones, William Ooko and the then managing director George Okungu as key players in the irregular release of petroleum to Triton.

KPC has since undergone a major shake-up in its executive suites and board pointing to some piecemeal implementation of the report’s recommendations.

KPC is currently being run by a crop of new managers headed by Selest Kilinda – the then chief manager in charge of finance and strategy who replaced George Okungu as managing director.

The company’s board has also been reconstituted and four new directors – Waithaka Kioni who served the company as deputy managing director, Alex Kazongo, Salim Ali and Bernard Kipkirui appointed.

Other board members are Joseph Kinyua (Treasury permanent secretary), Mr Kilinda, Rukia Subow, Joseph Ichunge Kinyua, and Wilfred Deche (alternate to Energy permanent secretary).

“There was direct involvement in administration of the CFA at a senior level and/or with assumed primary decision making authority,” the report says urging the board to act in line with the legal advice and the KPC’s internal procedures.

Unlock a world of exclusive content today!Unlock a world of exclusive content today!