Time flies with great content! Renew in to keep enjoying all our premium content.

Prime

How to reset the button for Kenya economic takeoff

BD GRAPHIC

Kenya’s slippage to macro-policy errors has bred a cottage industry of unflattering expert commentaries. As hatched in National Treasury, random missteps, degraded economic policy and advice now risk pushing Kenya to existential lows.

It is a brand and mindset less of top economics than “shoot first” cowboy bravado on spending and excessive debt that avoids prior scrutiny on growth and development results, let alone the morass of corruption and audited looting.

But low bandwidth economic policy bungling is not uncommon. And we can correct it. President Bush Sr. once called Reagan’s economics “voodoo economic policy.” Tax and trade policy errors pepper Donald Trump’s tweets. Unabashed, he hits out at the Fed (central bank) to salvage himself. The Fed holds firm.

A helter-skelter lack of firmness or capacity marks the Treasury’s brand weaknesses. It sets targets it does not meet, as per main economic indicators. It treats austerity as mere conversation. Development allocations go unspent or mutate to recurrent spending in lip service to development.

We also bungle existential projects such as Galana-Kulalu on food security. County Governors stage protests for taxpayer funds that some squander, ignoring own-revenue bases, or public services. Policy coordination with CBK’s monetary policy is laughable.

We misrepresent it when Treasury tosses CBK Eurobond proceeds to reserves: that renders CBK a cashier for repayments.

Worse, the interest rate cap argued in defence of private sector credit has mutated to bargain-floor borrowing (in T-Bills and bonds) for the government which sweeps taxpayer funds to commercial banks in redemptions. How will future generations repay debts from a contracting economy?

To some analysts, the chickens may have come home to roost. Since 2013, as we illustrate with data, we’ve sidestepped the hard policy choices and macro-frameworks needed for growth. Cumulative structural defects have emerged.

Whether one looks at our final demand or the supply side, consumption and imports now drive growth. Not investment, production or even net-exports. During 2013-2014, the blue-ribbon Parastatal Reforms Implementation Committee (PRIC) took a deep dive. It cracked the policy secrets of nations that rebuilt state-owned sectors from inefficient dens of corruption to industrial and manufacturing giants- in China, Singapore and Malaysia, among others.

RIC authored a global award-winning model of Kenya’s Sovereign Wealth Fund Bill-2014, (presented at New York Stock Exchange), a Bank Consolidation Plan, Primary Dealership system for government securities, all this in the in-tray.

“U” curve

Where rays of policy hope flicker, as in CBK, the fog of timidity or complacency despite Constitutional guarantees on central banking regulation standards is baffling: Why boast un-earned borrowed reserves. Or preside over commercial banks that, to the detriment of the economy, circumvent lending and interest rate laws with new fees and commissions on one hand and accumulation of government securities (more borrowing) on the other?

With such institutional diversions (and now the profiteering in mobile lending that has snagged so many into defaults) banks profit from customer deposits and frustrate financial intermediation. The CBK’s rate decisions are unworkable under such diversions.

Some already brace for a staggering “U” curve in Kenya’s medium-term, for lack of an easier economic concept. Over the “L” -shaped phase, expect economic contraction, downturn, mark-time.

The “L”-shaped dive is already under way in massive business downsizings, layoffs, a fall in NSE, stalled housing and construction, high non-performing loans, worsening trade deficits, and the scramble for space by global brands that edge out local business, often using own-imported inputs.

The current decline is self-inflicted. With corrections undertaken in the phase, the post-2022 economic outlook will improve. Macro-policies for regulation and repair exist. Kenya tried them in similar economic straits, and they worked.

To reboot growth up the “J” path and post-2022 prosperity, cut and switch fiscal expenditures to revamp private sector-led production. Avoid the debt trap. Choose macro-policy mix options; trim and trim again the tax-guzzling of Counties; require fiscal consolidation, discipline, and accountability. Rebuild revenues.

The dire alternative is stagflation that will break the economy- meaning high inflation, unemployment, and stagnant demand. It is not an option. Why? My Huffington Post article in 2017, co-authored with world-class observers, portrayed 40percent unemployment, a ticking time bomb.

We can reap a demographic dividend or fall victim. What is it? Working-age youth and women with smaller families will propel working-age population to 73 percent by 2050 to fuel GDP growth. Untapped, they can fuel social disruptions.

Down the “U” Curve: The “L”-shaped phase is thus a breathing space to bring the country back from the brink through restructured saving, investment, and production with policy re-emphasis on private-sector-led economic activity and austerity towards 2022.

Five risks, if not rectified, could ruin medium-term recovery after 2022:

1) Tame excessive public debt and borrowing, and criminalise revenue leakages, including plunder, mismanagement, and illicit (cross border) financial flows- in reported research, mis-invoicing in Kenya drained eight percent of total Kenyan government revenues in 2013;

2) Trim expenditures and fiscal deficits in the two-tier governments, including domestic borrowing— it’s a Kenyan tradition for banks to convert billions of customer deposits, even public deposits (on their liabilities side) into government securities (on their assets side) while shunning loans to businesses that are the heart of job creation today; we then applaud historic banks’ profits earned in a feeding frenzy on government interest paid to banks using both taxpayers’ and borrowed funds;

3)Reform planning of public finances to modern results-based frameworks for spending results and outcomes and shun habitual revenue and GDP over-projections;

4) Arrest State-owned sector hemorrhage of taxpayer shillings; and

5) implement fiscal consolidation matched to a monetary policy to engender a “growth-friendly” environment. We’ve done it before.

Restoring growth -2002-2012: Impeccable turnaround policies quelled Moi-era quagmires that had so shredded the economy by 2002 it clocked only 0.5percent GDP growth.

Domestic debt

Kenya carried the weight of total public debt at a record 78.3 percent of GDP in 2000. Kibaki’s government tamed excessive public debt as a constraint to investment and sovereign risk. Lending to the private sector was tepid and costly.

Policy errors of the 1990s saw banks gorging at the trough of high-yielding government T-bills and bonds. The new government drained the trough with austerity and effective debt management.

It cut domestic borrowing, cut expenditures and mobilised revenues. Weaned from domestic debt as a milk cow, banks marketed credit to the private sector- financial intermediation. Growth recovered.

The new Government applied appropriate macro-policies gliding public debt to a record low of 38.20 percent by 2012 in two broad phases. From 2002 to 2007, the government tightened the fiscal side while mobilising revenues; and it loosened monetary policy, helping increase credit to the private sector.

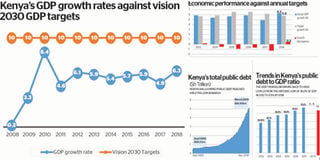

It did the latter by reducing domestic borrowing to crowd-in private sector credit which expanded. The policy mix ignited private sector-led GDP growth from 0.5 percent in 2002 to 2.9 percent, 5.1 percent, 5.9 percent, 6.5 perccent, and 6.8 percent, over 2003, 2004, 2005, 2006 and 2007, respectively. Kenya’s economic takeoff seemed assured.

Financial crisis and tribal clashes: The next phase centred on 2008-2009 when shocks of the global financial crisis and political crisis (tribal clashes) hit economic recovery. GDP growth in 2008 plunged to 0.2 percent. Government re-engaged pro-growth policies but with a new macro-policy framework.

The Government still favoured private sector-led growth, but it took advantage of the revenue mobilisation of the first phase to support growth from both the fiscal and monetary side.

It switched to a macro-policy mix of both easier monetary policy and expansionary fiscal policy.

GDP growth again surged from 0.2percent to 3.3 percent, and 8.4 percent over 2009 and 2010 (Kenya’s highest since 9.5 percent GDP growth in 1977).

Kenya’s elusive economic takeoff (a la Vision 2030) again seemed assured. The 2008-09 policy mix and success in re-igniting growth was whip-smart in global retrospect.

It replicated Barack Obama’s macro-policy in the US that revived the economy as the world tipped into recession. The Euro-zone, in contrast, chose austerity and delayed easing monetary policy. It’s yet to recover from economic contractions.

The 2010 peak of 8.4 percent GDP growth is the nearest we have come to closing the “Takeoff” gap towards annual target growth of 10 percent mandated in Vision 2030, and the Second Medium-Term Plan, 2013-2017 (themselves the creations of post-financial crisis economic policy in Kenya). The gap narrowed to 1.6 percent of the target in 2010.

Aborted takeoff since 2014? In review, recent decades of macro-policy mix thus prove that re-building growth, even from the ashes, is not rocket science.

The post-Kibaki era from 2013 faced challenges in devolution, with undisputed benefits, yet broken public finances and corruption. Wastage runs high. County elites live large on taxpayer’s money with little in own-revenues or devolved development. Counties’ mischief is endemic on accountability or public services. Though GDP growth tracked 6.1 percent and 5.9 percent, over 2012 to 2013, Kenya miscalculated and missed targets every year from 2014 to 2017.

Economic takeoff stalled and the debt treadmill and extravagance re-emerged. The debt pendulum swung back to high levels from the historic low of 38.2 percent of GDP in 2012: 57.1 percent by 2017 (over Sh5.4 trillion in March 2019, according to CBK).

A late brake on debt/GDP growth faces a historic paradox: forex reserves for debt repayments stacked at CBK track not the economic health or export earnings, but accumulated external borrowing (debt-funded reserves) and massive inflows of Diaspora remittances- itself an ignored potential for debt financing. Such liquidity can only be irrational and transitory. Pressures on inflation and the Kenya shilling could pile up.

If Kenya wants to create prosperity after 2022 and face threats of systemic economic decline, we have to press the re-set button on public finances and macro-policies.

Mbui Wagacha is a former senior economic adviser and acting chairman Central Bank of Kenya (CBK)

Unlock a world of exclusive content today!Unlock a world of exclusive content today!