Kenya is lagging her economic peers and regional neighbours in the performance of goods and services taxes due to many exemptions and compliance challenges, putting pressure on those paying income tax to shoulder the country’s revenue burden.

The World Bank estimates in a report titled Kenya Public Expenditure Analysis 2019 that Kenya is ceding tax revenue equivalent to 3.6 to 3.7 percent of GDP due to VAT exemptions.

The global lender also points at leakages in excise duty due to fake excise stamps as a problem area in hitting tax targets.

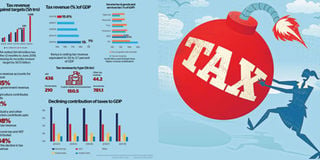

The ratio of VAT revenue to GDP for Kenya decreased from 4.5 percent of GDP in the 2014/2015 fiscal year to 4.1 percent in 2017/2018.

“Comparing Kenya’s revenue collection through VAT and excise taxes, the country has on average (over the period 2013-2017) lagged the performance levels in Rwanda and Uganda, as well as levels attained in aspirational economies such as South Africa, Vietnam, and Thailand,” says the World Bank in the report that was released in June.

Kenya’s volume of goods and services taxes as a percentage of GDP stood at 6.5 percent in the period between 2013 and 20-17, the World Bank calculations show, which is behind South Africa at 10.3 percent, Vietnam (8.8 percent), Thailand (8.5 percent), Rwanda (7.3 percent) and Uganda (7.2 percent).

On the other hand, income taxes as a percentage of GDP stood at about 8.2 percent in the period, second only to South Africa (14.8 percent) among the regional and income level peers.

The disparity is also a pointer to the shortcomings in the tax administration framework. Most income taxes are easier to collect for the Kenya Revenue Authority, especially pay-as-you-earn taxes that are deducted by employers before remittance of salaries.

VAT and excise duties are more prone to evasion, with the taxman often finding fake excise stamps worth billions of shillings in manufacturing plants.

Tax exemptions across the different tax categories have always presented a delicate balancing act for the National Treasury. Some are meant to encourage local production by making it cheaper to import raw materials or components for local assembly.

They can also be deployed to encourage investments into the country — as a means of attracting capital investors — in the race between States for scarce foreign direct investment.

On the other hand, there is pressure on the Treasury to maximise its revenue collection, especially in a country running a large budget deficit like Kenya.

This is more so when the country keeps missing its tax revenue targets, which has pushed the Treasury into borrowing that is fast spiralling towards unsustainable levels.

In the just ended 2018/2019 fiscal year, tax collection fell below the revised target of Sh1.5 trillion target (original target was Sh1.69 trillion) by Sh72.7 billion.

It continued a now familiar tale of tax revenue growth that is not satisfactory, especially with revenue targets that are often seen as unrealistically high. The total collection of Sh1.44 trillion was Sh100.1 billion higher than the revenue collected in the 2017/18 fiscal year.

Efforts by the Treasury to institute some measures of fiscal consolidation have been falling short, and, therefore, tax revenue has been unable to keep up with expenditure.

In the current fiscal year, the country’s spending is Sh3.01 trillion, and expects to collect Sh1.94 trillion in taxes, according to Treasury’s budget plan.

In the tax projection, income taxes, profits and capital gains are expected to contribute Sh884.4 billion, while taxes on goods and services will pump in Sh843 billion.

The remainder comes from taxes on international trade and transactions at Sh196.2 billion, and other taxes that will contribute Sh11.9 billion. Such lofty targets should, on paper, be attainable in an economy that is expected to grow at six percent.

The World Bank says however that the drivers of Kenya’s economic growth are not necessarily supportive of tax growth, hence the real growth rate of income tax is lower than the improvement in real GDP and historically the difference has been large.

“This could suggest that growth in Kenya’s economy could be emanating from sectors that are hard to net in terms of income tax (agriculture and informal sectors) which is in line with the hypothesis that structural change in Kenya’s economy in favour of agriculture has led to erosion of the effective tax base,” says the World Bank.

The growth in excise and import duties on the other hand appears to closely trace the growth in their tax bases (the final consumer of goods), even though the frequent changes in exemptions for various categories of goods and services have brought some volatility.

One result of the rise in share of GDP of agriculture has been a reduction in tax revenue as a share of GDP, from 18.1 percent 2013/2014 to 15.7 percent in 2017/2018. The contribution of agriculture to tax revenue is about two percent, the World Bank says, while more than 98 percent is attributed to industry and services sectors.

It means, therefore, that tax administration reforms meant to raise revenue performance, such as integration of iTax with other databases (IFMIS, and NHIF), rolling out of integrated customs management and expansion of tax base will require more time to achieve their goals.

Unlock a world of exclusive content today!Unlock a world of exclusive content today!