Time flies with great content! Renew in to keep enjoying all our premium content.

Prime

Safaricom future value linked to M-Pesa growth

A Nairobi-based M-Pesa agent attends to a client. Safaricom has reduced the voice component from 66 to 62 per cent of its revenue equalling Sh96.3 billion. Photo/FILE

Safaricom’s future value will depend on how the company’s mobile money transfer service M-Pesa performs in an increasingly competitive market, an investment bank’s analysis shows.

A valuation note on the company by Standard Investment Bank (SIB) released ahead of the company unveiling of full-year results says new battle ground for the telecommunications firm will be on electronic payments.

The SIB analysts say that while competition in voice, the cornerstone of its business, will increase as more firms eye the market, that will not be a serious threat to Safaricom.

Monday’s results, however, showed the firm had managed to reduce the voice component from 66 to 62 per cent of its revenue equalling Sh96.3 billion as its profit rose by over two-thirds.

“We do not feel these changes will pose any significant value-destroying competition. In fact, the main competitive focus is likely to lie in the payments space, which is being spurred by regulatory initiatives that focus on e-government,” says the note.

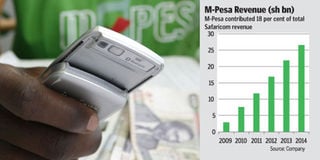

M-Pesa’s revenue increased by a respectable 22 per cent to Sh26.6 billion in the year ended March 31, 2014. The report notes that MTN and Viettel of the UK are reportedly looking into entering the Kenyan market, adding that their entry is unlikely to hurt revenues.

This is unlike August 2010 when Safaricom’s profitability and share price slumped after Zain (now Airtel) triggered a price war by slashing rates following the Communications Commission of Kenya’s lowering the mobile termination rate (MTR) from Sh4.42 to Sh2.21.

Investment banks and stockbrokers then lowered their valuation of Safaricom’s shares which saw the stock fall below the Sh5 initial public offering price.

“With these assumptions, our fair value declines from Sh6.20 to Sh4.85,” said a note released by Kestrel Capital as the tariff wars raged.

The MTR is set to fall again in June to Sh0.99 from Sh1.15, but there are no expectations that the scenario will be repeated this time round.

“This is unlikely to have a major impact on retail tariffs, in our view,” says SIB’s note.

The note says the fair value of Safaricom’s share is Sh12.53, just about what the share was trading at before the release of results.

The analysts had estimated net earnings at Sh24 billion, a billion more than the actual profit. The biggest threat going forward will be from companies eyeing the growing cashless payments market. Banks and independent money transfer firms are set to be the new competitors for Safaricom.

“A plan by Kenya Bankers Association to provide a real-time interbank money transfer platform is likely to create a real challenge to Safaricom’s M-Pesa service (one of the key advantages for M-Pesa has been real time settlement).

‘‘Ultimately, we still see most payment transactions being booked over the phone which means some revenue one way or another,” says the note.

Public Service Vehicles are also going cashless from June, which is expected to create another revenue stream for firms facilitating electronic payments.

“As at March 31, 2014 the service (Lipa na M-Pesa merchant payment tool) had 122,000 registered merchants, of which 20 per cent (24,137) were active on a 30 day basis,” said Safaricom CEO Bob Collymore on Monday.

Our priority this year is to commercialise this service by growing the number of active merchants and making Lipa na M-Pesa the preferred electronic payment platform.

‘‘This will make a significant contribution to the lives of our customers and accelerate Kenya towards a cash-lite economy.”

Unlock a world of exclusive content today!Unlock a world of exclusive content today!