When Members of Parliament convene this afternoon to vote on President Uhuru Kenyatta’s proposed austerity and tax measures, they will be choosing from an array of difficult options in a near do or die situation that has been gradually coming in the past five years.

At the centre of it all is a massive Sh870 billion debt service obligation that public finance experts say cannot be met without a significant increase in revenues.

The Sh870 billion debt servicing obligation means the country will spend more than 50 per cent of ordinary revenues – at best Sh1.6 trillion – to pay loans, leaving the rest to meet the huge financial obligations of both the national and county governments.

The revenue estimate is based on the fact that the country collected Sh1.487 trillion in the fiscal year that ended in June.

At 50 per cent, the debt servicing obligation is well over the 30 per cent threshold, putting Kenya in an even more precarious position.

In the financial year that ended in June, Nairobi spent Sh649.4 billion on debt servicing against total revenues of Sh1.487 trillion or 43.7 per cent, a huge increase from the 35.8 per cent the previous fiscal year.

Going back to the international market for new debt is seen as the only way Kenya can meet the looming heavy debt obligations without causing a crisis on the domestic front.

Mr Kenyatta’s quest to institute new revenue raising measures is therefore partly being seen as aimed at convincing potential lenders that Kenya can generate enough money in the future to service its debt obligations.

“With the maturity of debut five-year international sovereign bond in June 2019, we view the government will tap the international markets for a shorter-term Eurobond,” said Genghis Capital, an investment bank based in Nairobi.

Besides, the ongoing dilution of Kenya’s public finances has seen yields on the two Eurobonds rise, some by nearly 200 basis points (two percentage points) year to date.

This signals that the country could pay a much higher price if it went back to international markets for funds.

More recently, the global cost of money has risen in tandem with the US Federal Reserve decision to tighten its monetary stance with an increase of the base rate just before mid-June.

It remains to be seen how MPs will navigate this delicate terrain – on the one hand safeguarding the huge national interest that lies in protecting the integrity of the country’s finances – and reducing the economic pain that the new tax measures will visit upon those they represent.

Introducing new taxes is meant to help move total revenues closer to Treasury secretary Henry Rotich’s target of Sh1.9 trillion, which is required to finance the Sh2.9 trillion budget.

But there is also the drive to make deep spending cuts, which most MPs detest because it includes a cut in Constituency Development Fund (CDF)cash, the money that has become the biggest grassroots political tool and a slush fund for sitting parliamentarians.

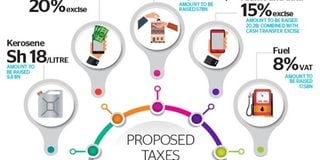

The list of tax measures Mr Kenyatta has proposed includes imposition of an eight per cent value added tax on fuel, excise duty on money transfer services, a housing development levy and an increase in tax on kerosene. Economist David Ndii says in an analysis of Kenya’s public finances that the tapping of syndicated loan markets could become necessary and at higher interest rates because the Treasury would be facing an unfavourable market environment and the Eurobond route might not be a realistic option.

Dr Ndii draws attention to the Sh102 billion that the national government had in July, but did not spend even as it disbursed nothing to the counties and for development, arguing the amount has been kept to form part of what is needed to refinance a maturing Sh250 billion debt.

“[T]he Sh102 billion shilling cash hoard — the money that government had but did not spend in July - is half the money that the government raised in the second Eurobond six months ago. It was not spent because it was raised to refinance the maturing debt. The balance has to be raised.”

The Treasury has proposed in the 2018/19 Budget to raise Sh1.949 trillion in revenues, a target that many analysts see as unrealistic given the rate at which revenues have been growing over the years.

In the fiscal year 2017/18, the Treasury realised just over 87 per cent of its projected revenues – meaning Sh1.7 trillion is the realistic amount even with the new tax measures.

“It is a stretch. I don’t think the Treasury can realise such revenues (Sh1.949 trillion). It needs to cut spending and among the places to look for is travel, both foreign and domestic,” said Churchill Ogutu, a research analyst with Genghis Capital.

Mr Ogutu said the Sh42 billion deficit in the first month of the fiscal year (July), if pro-rated for the whole financial year, signals that the Treasury would face a herculean task hitting its state targets.

Besides cutting expenditure, Mr Ogutu reckons the state could scale down spending on the “Big Four” agenda projects, especially that on housing.

“The housing development agenda is a low hanging fruit in terms of what the government can cut from its expenses this fiscal year. But it will need to do more than that and focus on priority projects as well as fiscal discipline,” he said.

Unlock a world of exclusive content today!Unlock a world of exclusive content today!