Time flies with great content! Renew in to keep enjoying all our premium content.

Prime

Barclays defies lending slowdown for 7.7pc profit growth

Incoming BBK managing director Jeremy Awori (left)and his predecessor, Mr Adan Mohamed, address the media after the release of 2012 results on Wednesday. Photo/Salaton Njau

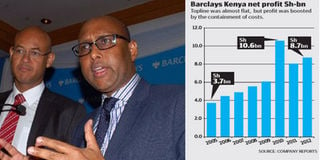

Barclays Bank of Kenya, the majority UK-owned financier, has registered a 7.7 per cent growth in net profit to Sh8.7 billion after slowing down credit expansion in the past year.

The loan book grew just 5.2 per cent as the mainly wholesale and corporate lender, which only some years back had attempted to aggressively enter the retail market, chose quality over quantity in loans issuance to preserve its conservative high-street culture of doing business.

Its non-performing loans as a fraction of its loan book shrunk to 0.1 from 1.3 per cent only two years ago as asset quality became the single most-important concern for the bank.

Just about five years ago, Barclays went on to open branches in places such as Githurai, regarded as a backstreet in banking within Nairobi, but many analysts now believe it was not as successful as it had hoped.

The trend in asset growth was seen as early as September 2012 when Barclays Kenya had the slowest growth among the top five banks in terms of net loans and advances.

“We expected a higher growth in the loan book but the bank was more cautious in terms of lending. It wants to avoid non-performing loans,” said Vimal Parmar, head of research at Burbidge Capital Ltd.

By last September, Barclays had chalked up 5.5 per cent growth in the loan book, only Sh5 billion more than at end of the same month in 2011.

During the same period, Equity Bank grew its loan book by 20 per cent or Sh22 billion to Sh131.37 billion, StanChart expanded its own by 7.6 per cent or Sh7 billion, while KCB grew it by eight per cent or Sh15 billion to Sh209 billion. Co-operative Bank also grew lending by 11 per cent to Sh118.2 billion.

With the credit manager’s office reserved for the most liquid and credit-worthy, the bank is unlikely to venture into resource-poor areas or increase its branch network.

The company’s total income grew only 4.1 per cent in 2012 and the only reason it was able to register a higher net profit was because its expenses rose at a slower pace of 1.0 per cent.

Due to the strengthening of the shilling during the year, the bank took a major hit on the foreign exchange earnings which fell by 8.9 per cent, pushing the total non-interest income down by 7.2 per cent to Sh9.3 billion.

In 2011, many banks recorded a profit on foreign exchange portfolio on the back of the volatility around the local currency, which depreciated to a historic Sh107 to the dollar in the month of October before appreciating thereafter.

Dividend fell drastically to Sh1 from Sh1.50 in 2011, on account of intentions by the bank to preserve cash for purposes of beefing up the company capital following new regulatory requirements on market and operations risk buffers.

“It will no longer be business as usual in so far as company dividends are concerned. With the new guidelines from the Central Bank on capital buffers, we don’t want to erode capital levels. We don’t want to give the money and then go back to the shareholders for it,” said Adan Mohamed, the bank’s outgoing managing director.

Mr Mohamed was presenting the 2012 financial results at InterContinental Hotel in Nairobi on Wednesday.