Investors in Treasury bills and bonds will no longer be able to make manual bids and payments for the securities at the Central Bank of Kenya (CBK) once the modernised Central Securities Depository (CSD) goes live from Monday.

The new CSD is an electronic over–the–counter trading platform that is meant to ease trading in the securities, improving liquidity and opening a more convenient avenue for Kenyans abroad to buy government debt.

The platform, known as CBK DhowCSD, is expected to tap more than Sh406 billion ($2.86 billion) from Kenyans abroad, who last year remitted a total of $4 billion (Sh569 billion) to the country.

A brochure on the new service by the CBK also shows that existing account holders, who have been bidding for securities manually or through the Treasury Mobile Direct service, will have their details transferred to the new CSD.

“CBK is discontinuing manual submissions/drop off of bids at its centres. Investors will no longer be able to submit manual bids to participate in auctions. Bids will be done through the DhowCSD,” said the CBK.

“CBK will no longer accept cash or cheque deposits for payments of Treasury bills and bonds—all payments will be made via a commercial bank.”

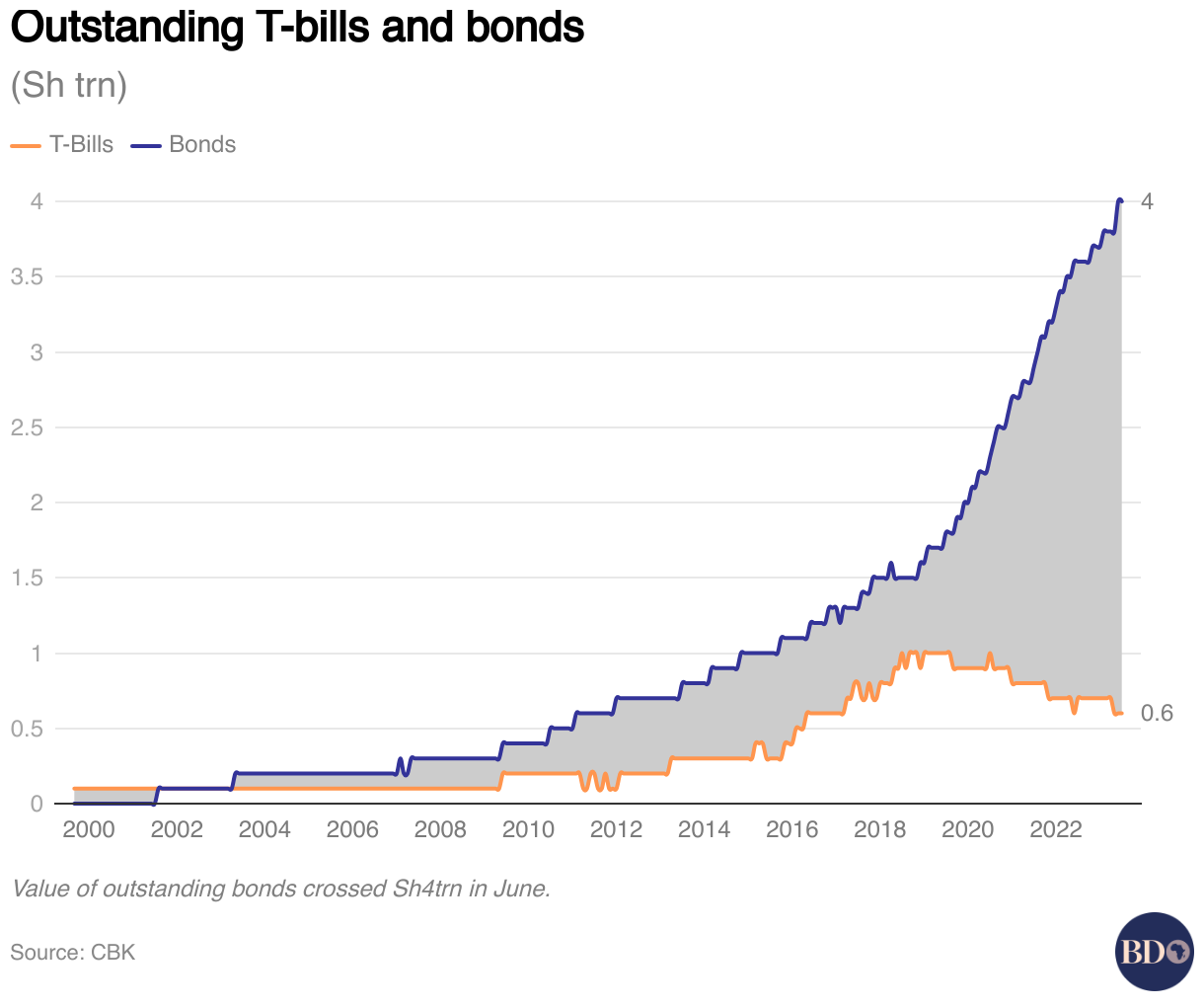

The government borrows from the domestic market through short-term Treasury bills, which are repayable within a year and longer-dated bonds, with the latter currently tradable on the Nairobi Security Exchange’s fixed income board.

T-bills, in the meantime, are not listed and can only be sold by rediscounting (selling them back to the Central Bank). The one-year T-bill is, however, tradeable in an OTC market at the CBK.

Work on the platform, funded by the World Bank Group, started around September 2020 and was expected to go live in June 2022.

Besides electronic trading capability, the new CSD is expected to improve pricing efficiency and transparency in securities trading thereby lowering yields.

The system will also enable banks to trade with one another by exchanging collateral of their treasury holdings, thus allowing smaller banks to get favourable interbank rates.

This form of horizontal repo is seen as key in rebalancing the interbank market, in which the large banks currently enjoy a large share of liquidity compared to their smaller peers.

Currently, small lenders get expensive interbank rates when borrowing from their big peers because they are considered risky and do not offer collateral for their overnight loans.

Big banks borrow from one another without collateral, confident in their balance sheets and potential to access additional funds from their shareholders.

Once the workings of the horizontal repo plan are refined, the banks will test how to allow their customers to borrow against their securities.