The banking and insurance industries are facing an ever changing regulatory environment, the latest being risk-based capital rules which are meant to strengthen governance in accounting for the institutions.

In the first quarter of this year, financial services firm Zamara carried out a survey on 17 bank and insurance chief executives to find out opportunities and challenges around regulation, product development and pricing, risk and expertise in the two industries.

The main regulatory issue facing banks and insurers this year is the introduction of the IFRS 9 and IFRS 17 accounting standards.

Banks have also been operating under a rate capping law since August 2016, which has put a squeeze on their interest margins.

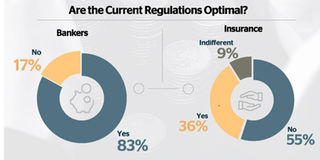

In the Zamara survey, which polled 11 insurance chief executives and six from banks, it emerged that the lenders are far more satisfied with their regulations compared to insurers.

Eighty three per cent of the bank executives said regulations in the sector were optimal, even as they expressed concern that rising capital requirements are likely to force some lenders to cut the scale of their operations.

On the other hand, just 36 per cent of their insurance counterparts said their regulations were optimal.

Their main concerns were that the new risk based capital requirements could end up stifling investment in the property and other asset classes, forcing them to formulate new investment strategies.

Insurers supplement their underwriting revenue with earnings from other investments such as equities and property. They are also concerned that the introduction of the IFRS 17 standard will force them to overhaul their operation model.

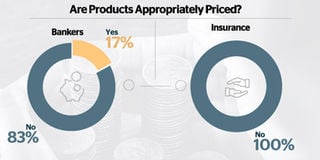

“None of the participants consider themselves fully prepared for the changes, and over half from each industry considered themselves to be 50 per cent or less prepared,” said Zamara in the report. On the issue of pricing of products, majority of those polled said that their markets had not priced their products appropriately. For banks, the challenge lay in the capping of interest rates chargeable on customer loans. Eighty three per cent of the CEOs said that the law had led to under-pricing of risk, reversing earlier views that risk was being overpriced when lending to customers.

They said that this had led to certain segments of the economy being locked out of the credit market, most notable SMEs which are considered very risky borrowers.

The bank executives also decried the lack of utilisation of big data to target and understand customers, pointing to deficiencies in the country’s credit rating system which has been accused of serving to punish bad borrowers and rewarding good ones. For insurers, concern on pricing revolved around high loss ratios arising from low premium charges on traditional insurance products.

All the chief executives polled from this sector agreed that their products were not appropriately priced.

The industry has been troubled by price undercutting for years, which causes revenue loss thus weakening the insurers’ ability to promptly settle claims.

It also leads to a negative perception of the industry among customers, making it difficult to grow insurance penetration above the current low level of about three per cent. The insurance executives also pointed out the lack of expertise in the industry, with 53 per cent saying that they were struggling in operations and technology.

Their main concern was on the shortage of actuaries and risk experts, which leads to lack of understanding of risks and the best methods of measuring and mitigating them. There is also a marked aversion to change in the industry, the executives said, which has put insurers at the risk of being left behind in a fast changing environment.

For instance, insurers have been slower in adopting mobile technology and payment methods compared to banks.

The lenders have aggressively adopted this technology, which has helped raise financial inclusion to above 75 per cent from 27 per cent just over a decade ago.

Bank executives unanimously agreed that there was sufficient expertise in the industry, even though there were a few concerns over their ability to meet emerging threats due to adoption of technology.

They said that the industry needs to bring in experts in disciplines such as IT, forensic audit, data analytics and derivatives — which will be introduced in the market soon.

The bank executives were also concerned about rampant poaching of staff by rivals instead of training their own, which has raised labour costs.